Social Security: Universal or selective? (1971) – with Milton Friedman …

Is Social Security Worth Its Cost?

Authors:Kevin Dayaratna, Rachel Greszler and Patrick Tyrrell

SUMMARY

KEY TAKEAWAYS

This report compares what Social Security can provide and what workers could receive if they had ownership of their Social Security payroll taxes.

This information can help individuals of all ages understand what they can expect to receive from Social Security or from private savings.

Virtually all Americans would be better off keeping their payroll taxes and saving them in private retirement accounts.

Social Security began as an anti-poverty insurance program, aimed at preventing workers from outliving their savings when they were no longer physically able to work. As such, Social Security was limited in nature, beginning as only a 2 percent payroll tax—and promising to never take more than 6 percent of workers’ pay. Today, Social Security’s Old Age and Survivors Insurance (OASI) retirement program takes 10.6 percent of workers’ pay, and its Disability Insurance (DI) program takes another 1.8 percent, for a combined total of 12.4 percent. This is more than most Americans pay in income taxes.

As Social Security has grown in size and scope, it has become more than just an insurance and poverty prevention program—and with millions of seniors living below the federal poverty line, it is not doing a great job even at that. Having reduced the incentive to save for retirement, Social Security now represents a significant portion of most workers’ retirement savings. Despite the fact that Social Security was intended to be an insurance program, providing a secure retirement income, individuals have no legal claim to their scheduled Social Security benefits, as the program can only pay out as much money as it has on hand and Congress can change benefit levels if it wants. Not surprisingly, more than 60 percent of workers under the age of 50 do not think Social Security will be able to pay them a benefit when they retire.

With Social Security consuming such a large component of workers’ paychecks and offsetting their own private savings, it is important that workers receive a valuable benefit from Social Security—one at least as good as they, as a whole, could obtain from saving on their own. This analysis looks across the United States and across generations to see if Social Security does in fact provide that.

Get exclusive insider information from Heritage experts delivered straight to your inbox each week. Subscribe to The Agenda >>

Utilizing federal government data on life expectancy and earnings in each state, Heritage analysts found that:

- On average, personal retirement savings significantly outperform the current Social Security system. Taking an average of all 50 states and the District of Columbia, the average worker receives significantly less from Social Security than he would have if he had conservatively invested his Social Security payroll taxes in the market.

- Foregone benefits vary across generations.For average-earner males in Florida (a median-income state), lost investment earnings equal over $600,000 for those born in 1955; over $700,000 for those born in 1975; and over $1.1 million for those born in 1995. For average-earner females living in Florida, Social Security will provide over $190,000 less in lifetime income than personal savings for those born in 1955; over $230,000 less for those born in 1975; and over $420,000 less for those born in 1995. (See Appendix Tables.)

- Individuals with lower life expectancies often lose greatly. This occurs because they receive little or nothing in benefits and cannot pass along all their lost contributions to their surviving family members. Consequently, certain areas of the country, including Washington, DC, have significantly lower returns from Social Security.

- Younger workers face lower, and even negative, returns from Social Security compared to older workers. This comes as a result of paying higher average Social Security tax rates over their lifetimes, coupled with a two-year increase in Social Security’s normal retirement age—as well as the benefit cuts that will occur if Social Security’s trust fund runs dry.

To see if Social Security is a worthwhile program for Americans—across generations and states—researchers at The Heritage Foundation’s Center for Data Analysis created a statistical model, The Heritage Foundation Social Security Rate of Return Model, to examine Social Security’s costs and benefits. We compare these results to what workers would have earned (including estimates on what younger workers likely would earn) in personal retirement savings accounts.

Social Security: Origin and Intent

Established during the Great Depression in the 1930s as part of President Franklin Delano Roosevelt’s New Deal, Social Security is a federal program designed to protect against poverty in old age. At that time, Social Security’s eligibility age of 65 was higher than the average life expectancy.1

Centers for Disease Control, “United States Life Tables, 1998,” National Vital Statistics Reports, Vol. 48, No. 18 February 7, 2001, Table 11, https://www.cdc.gov/nchs/data/nvsr/nvsr48/nvs48_18.pdf (accessed April 20, 2018).

Social Security’s payroll tax began at a rate of 2 percent and was never intended to rise above 6 percent.2

Social Security Administration, “Social Security and Medicare Tax Rates,” https://www.ssa.gov/OACT/ProgData/taxRates.html (accessed October 3, 2016).

Those taxes seemed sufficient because life expectancy was 17 years lower then than it is today; not many people lived long enough to collect benefits, and those who did collected them for less time than retirees today.3

Life expectancy for men in 1935 was 59.42 years compared to 76.07 in 2016; for women it was 63.32 years in 1935 compared to 80.45 years in 2016. See Felicity C. Bell and Michael L. Miller, Life Tables for the United States Social Security Area: 1900–2100, Social Security Administration, Table 10, pp. 162–166, https://www.ssa.gov/oact/NOTES/pdf_studies/study120.pdf (accessed April 20, 2018).

However, what started out small has morphed into a nearly $1 trillion annual program that redistributes income to 61 million people—or about one out of every five people in the United States (including about 50 million OASI beneficiaries and 11 million DI beneficiaries).4

Social Security Administration, The 2017 Annual Report of the Board of Trustees.

When Social Security first began, there were 42 workers paying into the system for every one retiree receiving retirement checks. Today, there are only 3.4 workers per OASI beneficiary.5

Ibid., Table IV.B3, p. 61.

The program has long been on an unsustainable path and will run out of funds to pay promised benefits in 2029 according to the Congressional Budget Office6

Congressional Budget Office, “CBO’s 2016 Long-Term Projections for Social Security: Additional Information,” Exhibit 8, p. 9, https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/52298-socialsecuritychartbook.pdf (accessed April 20, 2018).

and in 2035 according to the Social Security Trustees.7

Social Security Administration, The 2017 Annual Report of the Board of Trustees.

Absent reforms, benefits will decline by over 20 percent across the board after the Trust Fund runs dry.8

Ibid.

Knowing the estimated benefits workers will get from Social Security versus what they could get by saving on their own can help workers and policymakers better assess what types of Social Security reforms would be most beneficial.

Social Security’s payroll tax consumes 12.4 percent of workers’ paychecks (10.6 percent for the OASI program and 1.8 percent for the DI program)—but that is not enough to sustain the programs.9

For the period between 2016 and 2018, 0.57 percent of the 10.6 percent OASI , or retirement, program payroll tax is being reallocated to the DI program, meaning the OASI payroll tax is temporarily 10.03 percent and the DI tax is 2.37 percent. However, for the purposes of this analysis, we assume that the OASI payroll tax remains constant at 10.6 percentage points and the DI tax remains constant at 1.8 percentage points. See Social Security Administration, “Social Security Tax Rates,” https://www.ssa.gov/oact/progdata/oasdiRates.html (accessed October 14, 2016).

Maintaining current benefit levels for both OASI and DI would require the payroll tax to rise to 15.33 percent.10

Social Security Administration, The 2017 Annual Report of the Board of Trustees, Table IV.B5, p. 70. Although the stated actuarial deficits for the OASI and DI are 2.59 percentage points and 0.24 percentage points of taxable payroll (a combined total of 2.83), the Social Security Trustees note that the combined OASDI payroll tax would have to rise by 2.93 percentage points because of behavioral responses. We distribute the additional 0.10 percentage point increase proportionally across the OASI and DI programs, resulting in tax increases of 2.68 percentage points and 0.25 percentage points, respectively.

Unfortunately, the payroll tax reduces workers disposable incomes and provides many with an incentive to save less. Therefore, a significant percentage of older individuals today rely primarily on Social Security for retirement income.11

More than 33 percent of aged beneficiaries receiving Social Security benefits had less than 10 percent additional income to their social security checks during retirement. Social Security Administration, “Income of the Aged Chartbook, 2014,” https://www.ssa.gov/policy/docs/chartbooks/income_aged/2014/iac14.html#chart9 (accessed July 29, 2016).

Because Social Security no longer functions primarily as a poverty-prevention program for individuals who are too old to work, and since it consumes so much of workers’ savings capacity, it is important to quantify whether or not Social Security is a valuable savings program.

Why Rates of Return Matter

“Rate of return” is a widely used metric to measure the performance of an investment—that is, how much a given dollar returns over a specified period of time. If $100 invested today is worth $110 in one year, then it has a 10 percent annual rate of return that year. Since workers contribute payroll taxes and expect to receive something in return, Social Security is considered an investment by many people.

In reality, however, Social Security is not an investment. For starters, today’s cash-flow deficits within the program mean that all incoming payroll taxes go immediately out the door to pay promised benefits. Moreover, Congress ultimately determines what workers pay into the system and receive from it—leaving workers with no control.

Social Security’s rate of return, or what workers get back in comparison to what they pay in, is entirely determined by Social Security’s benefit calculation formula as well as its Trust Fund assets. Consequently, the “returns” individuals receive from their Social Security contributions vary wildly across individual workers and across generations. While Social Security provided a high return on payroll taxes to its early beneficiaries, it promises a much lower return to future beneficiaries—and, under certain scenarios, the actual return that it can currently afford to pay to millions of future retirees can even be negative.

We used the Heritage Foundation Social Security Rate of Return Model to compute the program’s internal rate of return under two scenarios: (1) current law (which assumes the trust fund runs dry in 2035 and benefits are cut by over 20 percent);12

Social Security Administration, The 2017 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, Table IV.B1, p. 54.

and (2) maintaining promised benefits through an across-the-board payroll tax increase. Although some individuals do not live long enough to collect Social Security benefits, we only report rates of return for those who live to at least age 66 (the current full, or normal retirement age). Consequently, our results overstate Social Security’s actual rate of return because they exclude individuals who die before age 66 and receive little, if anything, in return for their Social Security contributions.13

Unlike a retirement account that can be passed on, the Social Security death benefit consists of just $255.00. Social Security Administration, “Frequently Asked Questions: Who Can Get a Lump-Sum Death Benefit?” https://faq.ssa.gov/link/portal/34011/34019/Article/3768/Who-can-get-a-lump-sum-death-benefit (accessed August 21, 2017).

We compare these Social Security returns to a third scenario in which workers are hypothetically able to invest their payroll taxes in private accounts made up of stocks and bonds, as opposed to relying on benefits paid from other workers. These private account simulations assume that workers conservatively invest 50 percent of their existing payroll taxes in federal government bonds and the other 50 percent in large stocks.14

Large stocks are based on those of the Standard & Poor’s (S&P’s) 500 Composite index as used in Roger G. Ibbotson, 2017 SBBI Yearbook: Stocks, Bonds, Bills, and Inflation: U.S. Capital Markets Performance by Asset Class, 1926–2016 (Hoboken, NJ: John Wiley and Sons, Inc., 2017), Chapter 4. Returns for large stocks are the inflation-adjusted capital gains or losses plus reinvested dividends of large-cap stocks as reported therein. Government bonds are those used by Ibbotson to calculate annual returns on long-term government bonds, and usually consist of 20-year treasury bonds.

We applied historical rates of return for stocks and bonds through 2016 and projected forward the historical average (from 1954–2016) for 2017 and beyond (2.75 percent for government bonds and 7.04 percent for large-cap stocks). Full details are available in our methodological appendix.

Key Assumptions and Methodology of Heritage Foundation Social Security Rate of Return Model15

See, infra, “Appendix: Basic Assumptions and Methodology,” for a more complete explanation of the methodology of these calculations.

This analysis utilized the Heritage Foundation’s Social Security Rate of Return Model, which incorporates the following assumptions:

- The hypothetical amount invested in personal retirement savings accounts equals Social Security’s payroll tax, which is 10.6 percent under current law (which requires benefit cuts beginning in 2035 to maintain solvency of the Social Security Trust Fund), and 13.28 percent under a financially solvent system that can maintain “promised” benefits. We do not make any changes to Social Security’s Disability Insurance (SSDI) program in this exercise, nor do we include the 1.8 percentage point SSDI payroll tax in workers’ hypothetical personal retirement account contributions.

- We display results separately for both male and female individual workers with: (1) average earnings; (2) 50 percent of average earnings; and (3) the taxable maximum ($127,200 in 2017).

- For state-by-state analysis, we make use of the fact that average incomes and life expectancies vary by state.

- We account for future increases in life expectancy and wages. Unless otherwise stated, we use the intermediate assumptions reported in the Social Security Trustees’ 2017 annual report.16

Social Security Administration, The 2017 Annual Report of the Board of Trustees, Table VI.G6, pp. 216–217. AWI for years not presented in the five-year forecast were interpolated based on the growth rates of these forecasts themselves.

- We adjust all Social Security benefits for inflation according to the Social Security Administration’s use of the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). For discounting previous and future values of wages, investments, and returns, we use the Consumer Price Index for All Urban Consumers (CPI-U) to remain consistent with our source for inflation-adjusted returns (2017 SBBI Yearbook).17

Ibbotson, 2017 SBBI Yearbook, Chapter 4.

We use the Congressional Budget Office’s January 2017 projections for future inflation in the CPI-U.18

Congressional Budget Office, “The Budget and Economic Outlook: 2017 to 2027,” January 24, 2017, p. 54, https://www.cbo.gov/publication/52370 (accessed May 5, 2017).

- We include both the employee’s and employer’s shares of payroll taxes in the calculations.19

We do not address taxation issues upon withdrawal of retirement funds. We treat investments in personal savings accounts the same as payroll taxes under current law, meaning the employee portion of taxes is not tax deductible (Roth treatment), while the employer portion is tax deductible. Both these accounts, as well as some Social Security benefits, may be subject to post-retirement income taxes.

- The rate of return on private investments listed in the tables assume a conservative mix of 50 percent large-cap U.S. stocks and 50 percent U.S. Treasury bonds. We also provide information about how much workers pay in OASI payroll taxes over their careers and how much they receive in Social Security benefits (assuming they live the average life expectancy), compared to how much they could have accumulated in a private retirement account had they invested their payroll tax dollars.

National Analysis

We used the Heritage Foundation Social Security Rate of Return Model to determine how American workers born in 1995 and with differing life expectancies fare in terms of the expected rate of return they receive from Social Security (the amount they receive from Social Security compared to what they paid in payroll taxes, all in 2017 dollars):

These results illustrate that Social Security provides extremely poor—often negative—rates of return for younger workers all across the country, especially for individuals with lower life expectancies. In comparison to the current system, private retirement accounts would provide significantly higher returns to Americans, regardless of their life expectancies.

State-by-State Analysis

We also used The Heritage Foundation Social Security Rate of Return Model to conduct a state-by-state analysis of the rate of return of Social Security versus a hypothetical simulation assuming payroll taxes used for Social Security were instead invested in private accounts. The following tables provide, by state of residence, the rate of return of Social Security compared to private accounts.

These tables, as well as the more detailed tables in our appendix, show workers’ estimated total lifetime Social Security benefits compared to their accumulated personal retirement account balances under two scenarios—tax increases or benefit cuts—that would make Social Security solvent over the long run. We also break total benefits and accumulated account balances down into monthly benefits and monthly annuities that workers could purchase using their personal retirement account balances. For both measures, we show workers by state, gender, and income level:

Our results demonstrate that younger workers (born in 1995) of all income levels would receive between two and seven times as much in retirement income from personal savings as they would from Social Security. Because Social Security paid out more in benefits than it collected in tax revenues to earlier generations, the gains would not be as large for older workers (those born in 1955 and 1975); however, they would still receive more from personal retirement accounts than from Social Security.

Why Private Savings Produce Higher Retirement Incomes than Social Security

Our results establish that personal investment accounts provide a significantly greater rate of return compared both to what Social Security can afford to pay as well as what it has promised to pay. Prior research comes to the same conclusion.20

Davis and Lacoude, What Social Security Will Pay. See, for example, Thomas A. Garrett and Russell M. Rhine, “Social Security Versus Private Retirement Accounts: A Historical Analysis,“ Federal Reserve Bank of St. Louis Review, Vol. 87 (March/April 2005), pp. 103–121, https://research.stlouisfed.org/publications/review/05/03/part1/GarrettRhine.pdf (accessed September 30, 2016), and Michael Tanner, “Still a Better Deal: Private Investment vs. Social Security,“ CATO Institute Policy Analysis No. 692, February 13, 2012, http://www.cato.org/publications/policy-analysis/still-better-deal-private-investment-vs-social-security (accessed October 4, 2016).

1. Higher Returns and Larger Retirement Incomes. Investment returns in the private market are two to three times the rate of return of U.S. Treasuries (what Social Security used to invest in when it ran surpluses). Consequently, even most low-income earners who get the most back from Social Security (relative to what they contribute) would end up with higher retirement incomes if they had personal investment accounts. This phenomenon was not always true in the past under Social Security’s unsustainable promises, but it is true for anyone in their 40s or younger today.

For example, a 23-year-old female, born in 1995, living in Florida and earning the average wage can expect a monthly Social Security check of $1,393 in 2017 dollars when she retires at age 67 in 2062. However, if her payroll taxes had been invested half in large-cap stocks and half in Treasury bonds, based on historical averages she could buy an inflation-adjusting annuity (similar to Social Security) that would provide $2,524 per month in year 2017 dollars.21

The single female earner in Florida would have $709,461 saved at retirement in 2017 dollars. If she purchased an annuity paying her a monthly payout until death, which adjusts for CPI-U each year, it would pay her an estimated $2,524 in monthly income in 2017 dollars. Rate is based on ImmediateAnnuities.com annuity quotes in effect October 21, 2016, https://www.immediateannuities.com/ (accessed May 5, 2017).

This amount represents almost twice the amount Social Security will be able to pay.

The same is true for other earners. A 23-year-old male, born in 1995, living in Florida and earning only half the average wage throughout his working years would accumulate enough in a personal account to receive an annuity that would pay $3,093 per month in 2017 dollars. Social Security can only provide him significantly less at $1,551 per month.22

The single male earner in Florida would have $781,910 saved up at retirement in 2017 dollars. If he purchased an annuity paying him a monthly payout until death, which adjusts for CPI-U each year, it would pay him an estimated $3,093 in monthly income in 2017 dollars. Rate is based on ImmediateAnnuities.com annuity quotes in effect October 21, 2016, https://www.immediateannuities.com/ (accessed May 5, 2017).

Even low-earning females (born in 1995) who tend to receive the most bang-for-the-buck from Social Security would receive 40 percent more from a personal account than from Social Security ($1,262 per month from a personal account vs. $902 from Social Security).

2. Continued Wealth Growth Post-Retirement.A second advantage of private retirement savings is that savings that are not withdrawn at retirement can continue to earn investment returns during retirement. Even with conservative investments, savings can continue to grow and provide for larger disbursements in subsequent years and bequests to help support family members, friends, or charities after death.

3. The Ability to Leave Bequests. Social Security prevents workers from passing on their “saved” payroll taxes to their heirs if they die before collecting benefits or shortly afterwards. Under the current system, a mean-income worker pays about $4,700 per year into Social Security’s retirement program.23

In the first quarter of 2017, the mean usual weekly earnings of full-time wage and salary workers was $855. This translates into $44,460 annually and would amount to $212,074 over a 45-year career, assuming the worker begins at age 22 and retires at age 67. Mean earnings come from U.S. Department of Labor, Bureau of Labor Statistics, “Table 1: Mean Usual Weekly Earnings of Full-Time Wage and Salary Workers by Sex, Quarterly Averages, Seasonally Adjusted,” https://www.bls.gov/news.release/wkyeng.t01.htm (accessed June 29, 2017).

Over a 45-year career, that is up to $212,000 that he could potentially lose if he dies before collecting benefits. Personal savings, on the other hand, do not disappear if their owners die before using them. Shifting some or all of Social Security’s taxes to personal savings could have a particularly large and positive impact on lower-income earners as well as on many other groups that tend to have lower life expectancies and are more likely to get little to nothing back from their Social Security taxes. Bequests can serve as more than windfall benefits; they can change individuals’ and families’ lifetime trajectories by providing money that can help a child or grandchild attend college, start a business, or make other investments in their futures.

4. Larger Paychecks, Greater Incomes, and Increased Wealth. Social Security could accomplish the goal of preventing poverty in old age with significantly lower taxes than it currently extracts. A smaller Social Security program would leave workers with bigger paychecks that they could use for current consumption, gaining education, pursuing business opportunities, building wealth, and generating higher retirement incomes. More income and wealth would make low- and middle-income communities more dynamic and prosperous places to live and work.

5. Increased Productivity. Personal savings that support private investments allow companies to create productivity-enhancing capital in the form of new machines, technology, and facilities. This increases the output of workers, which leads to better jobs and higher wages.24

For a discussion of what capital is and how it increases output, see Marginal Revolution University, “Physical Capital and Diminishing Returns,“ http://www.mruniversity.com/courses/principles-economics-macroeconomics/law-diminishing-returns-marginal-product-capital (accessed June 29, 2016). For a discussion of how workers’ income increases when the supply of capital increases, see James Sherk, “Labor’s Share of Income Little Changed Since 1948,“ Heritage Foundation Backgrounder No. 3111, May 31, 2016, http://www.heritage.org/research/reports/2016/05/labors-share-of-income-little-changed-since-1948.

The current Social Security system—which immediately spends all incoming revenues on retirees’ benefits—fails to accomplish the same productivity- and opportunity-enhancing effects.

Conclusion

This report provides workers with a comparison between what Social Security can provide and what they could receive if they had ownership of their Social Security payroll taxes. This information can help individuals of all ages understand what they can expect to get from the program in the long run.

The results are overwhelmingly clear. Americans would be better off keeping their payroll tax contributions and saving them in private retirement accounts than having to sacrifice them to the government’s broken Social Security system. Social Security’s design has, over the decades, presumed that many Americans are too incompetent to make informed decisions for themselves, but few Americans believe that the government knows better than they do what is best for them and their families. Moreover, Social Security’s financial structure effectively guarantees that workers will receive extremely low, or even negative, returns on their payroll taxes.

—Kevin Dayaratna, PhD, is Senior Statistician and Research Programmer in the Center for Data Analysis, of the Institute for Economic Freedom, at The Heritage Foundation. Rachel Greszler is Research Fellow in Economics, Budget, and Entitlements in the Thomas A. Roe Institute for Economic Policy Studies of the Institute for Economic Freedom. Patrick Tyrrell is Research Coordinator in the Center for International Trade and Economics of the Kathryn and Shelby Cullom Davis Institute for National Security and Foreign Policy, at The Heritage Foundation.

—

The Real (and Growing) Problem with Social Security

In an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other nations.

But we’re not in that ideal world. We are forced to participate in a Ponzi Scheme known as Social Security.

But we’re not in that ideal world. We are forced to participate in a Ponzi Scheme known as Social Security.

By the way, that’s not necessarily a disparaging description. A Ponzi Scheme can work if there are always enough new people in the system to pay off the old people.

But because of demographic changes (increasing lifespans and decreasing birthrates), that’s not what we have in the United States.

And this is why Social Security faces serious long-run problems.

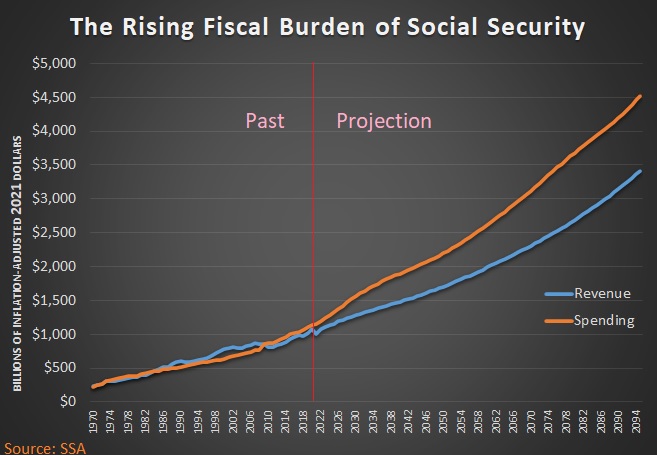

How serious? The Social Security Administration finally released the annual Trustees Report. This document has a wealth of data on the program’s financial condition, and Table VI.G9 is where the rubber meets the road.

As you can see from this chart, there will be an ever-increasing burden of Social Security taxes and spending over the next 75 years. And these numbers are adjusted for inflation!

The good news (relatively speaking) is that the economy also will be growing over the next 75 years, both in nominal terms and inflation-adjusted terms.

The bad news is that spending on Social Security will grow at a faster rate, so the program will consume a larger share of the economy’s output.

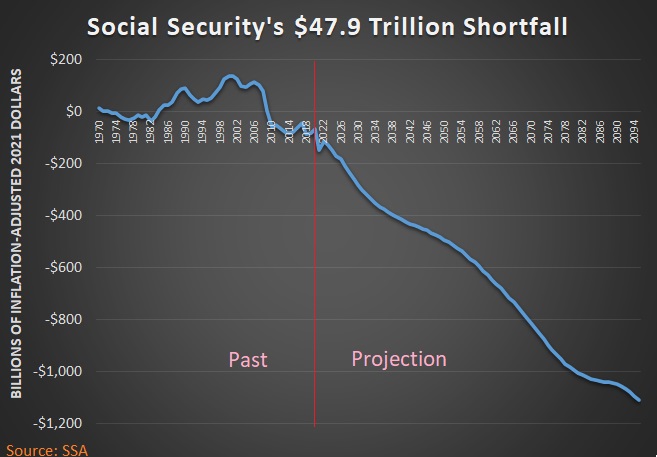

And because Social Security spending is growing faster than the economy (and also faster than tax revenue), this next chart shows there is going to be more and more red ink in the future. Once again, you’re looking at inflation-adjusted data.

As indicated by the chart’s title, the cumulative shortfall over the next 75 years is nearly $48 trillion. That’s a lot of money, even by Washington standards.

And with each passing year, the problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 report.

I’ll conclude by observing that today’s column focuses on the big-picture fiscal problems with Social Security.

I’ll conclude by observing that today’s column focuses on the big-picture fiscal problems with Social Security.

But let’s not forget the program’s second crisis, which is the fact that Americans are deprived of the ability to enjoy much higher levels of retirement income.

Certain groups are particularly harmed by this aspect of the current program, including minorities, women, older workers, and low-income workers.

P.S. Our friends on the left argue that the program’s fiscal problems (the first crisis) can be solved with tax increases. Perhaps that is true, but it will mean a weaker economy and it will exacerbate the second crisis by forcing workers to pay more to get less.

P.P.S. I once made a $16 trillion dollar mistake on national TV when discussing Social Security’s shaky finances.

P.P.P.S. Much of the news coverage about the Trustees Report has focused on the year the Social Security Trust Fund supposedly runs out of money. But this is sloppy journalismsince the Trust Fund has nothing but IOUs (as illustrated by this joke).

America’s Future Fiscal Crisis Can Be Averted

I’m not optimist about America’s fiscal future. Thanks primarily to entitlement programs, the long-run outlook shows an ever-increasing burden of government spending.

And rather than hit the brakes, Biden wants to step on the gas with new giveaways, especially his plan to gut Bill Clinton’s welfare reform by creating new per-child handouts that would subsidize idleness and family dissolution.

But that doesn’t mean the problems can’t be fixed. We simply need to replace fiscal profligacy with spending restraint.

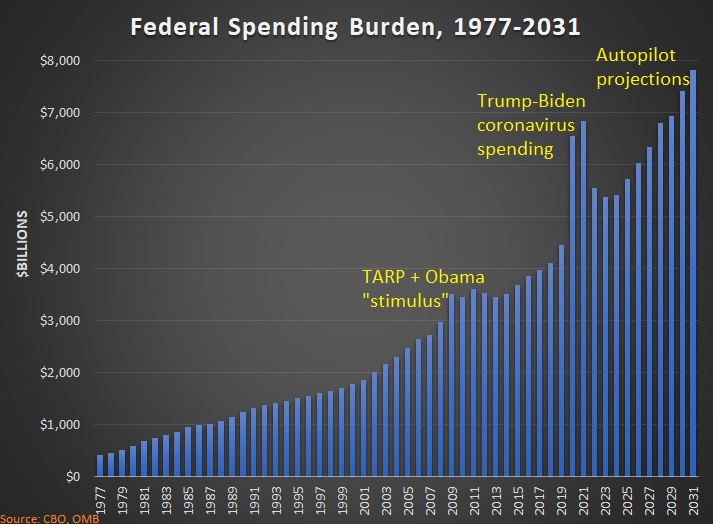

To set the stage for this discussion, here’s a look at what’s happened to the budget over the past several decades. You can see how the burden of federal spending has steadily increased, with noticeable one-time bumps in 2008-2009 (TARP and Obama’s so-called stimulus) and 2020-2021 (coronavirus).

The chart also includes projections between 2021 and 2031, based on new numbers from the Congressional Budget Office.

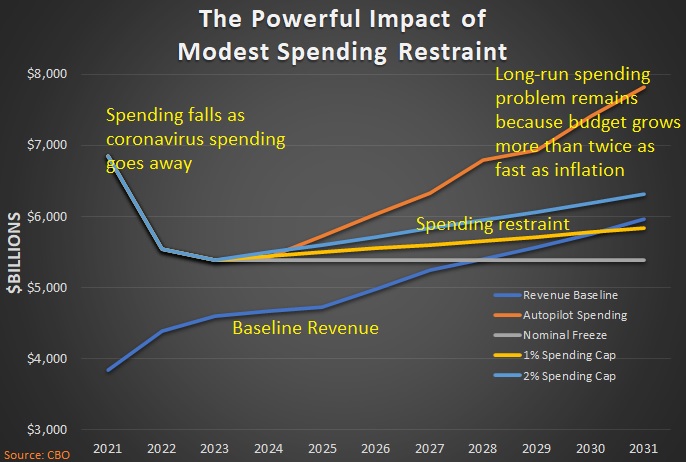

For today’s column, I want to focus on the next 10 years and show how the current fiscal mess can be averted with some modest spending restraint.

This second chart shows that spending actually drops over the next two years as coronavirus-related spending comes to an end. But once we get to 2023, the orange line shows that “baseline” spending (what happens to the budget if things are left on autopilot) climbs rapidly, more than twice the rate needed to keep pace with inflation.

But if there’s any sort of fiscal restraint (a freeze or some sort of spending cap), then the numbers look much better.

More specifically, a freeze or a 1-percent spending cap would actually produce a budget surplus by the year 2031.

But I’m not fixated on getting to a balanced budget. What’s more important is that the burden of government spending shrinks when the budget grows slower than the private sector.

In other words, we get good results when policy makers follow fiscal policy’s Golden Rule.

P.S. While it’s difficult to convince politicians to support spending restraint, it’s worth noting that the nation enjoyed a five-year spending freeze between 2009-2014.

P.P.S. In the long run, a spending freeze almost certainly requires genuine entitlement reform.

Open letter to President Obama (Part 712)

(Emailed to White House on 6-25-13.)

President Obama c/o The White House 1600 Pennsylvania Avenue NW Washington, DC 20500

Dear Mr. President,

I know that you receive 20,000 letters a day and that you actually read 10 of them every day. I really do respect you for trying to get a pulse on what is going on out here.

The federal government debt is growing so much that it is endangering us because if things keep going like they are now we will not have any money left for the national defense because we are so far in debt as a nation. We have been spending so much on our welfare state through food stamps and other programs that I am worrying that many of our citizens are becoming more dependent on government and in many cases they are losing their incentive to work hard because of the welfare trap the government has put in place. Other nations in Europe have gone down this road and we see what mess this has gotten them in. People really are losing their faith in big government and they want more liberty back. It seems to me we have to get back to the founding principles that made our country great. We also need to realize that a big government will encourage waste and corruption. The recent scandals in our government have proved my point. In fact, the jokes you made at Ohio State about possibly auditing them are not so funny now that reality shows how the IRS was acting more like a monster out of control. Also raising taxes on the job creators is a very bad idea too. The Laffer Curve clearly demonstrates that when the tax rates are raised many individuals will move their investments to places where they will not get taxed as much.

______________________

Published on May 19, 2013

What is the debt ceiling and why does it matter? Find out:http://BankruptingAmerica.org/DebtCei…

Congress’s dance with the debt limit can be confusing and, frankly, the details can be a real snooze fest for many Americans. Sometimes a little humor clarifies the absurdities of Washington antics better than flow charts and talk of trillions.

The 31-second video and accompanying infographic “The Debt Ceiling Explained” by Bankrupting America offers the facts, leavened with a dose of levity. The conclusion is serious, however: The country’s debt threatens economic growth, and spending cuts are the answer.

_________________________

I want to thank you for taking the time out of your busy day to respond to my earlier letter to you on this same subject.

It is obvious to me that if President Obama gets his hands on more money then he will continue to spend away our children’s future. He has already taken the national debt from 11 trillion to 16 trillion in just 4 years. Over, and over, and over, and over, and over and over I have written Speaker Boehner and written every Republican that represents Arkansans in Arkansas before (Griffin, Womack, Crawford, and only Senator Boozman got a chance to respond) concerning this. I am hoping they will stand up against this reckless spending that our federal government has done and will continue to do if given the chance.

Why don’t the Republicans just vote no on the next increase to the debt ceiling limit. I have praised over and over and over the 66 House Republicans that voted no on that before. If they did not raise the debt ceiling then we would have a balanced budget instantly. I agree that the Tea Party has made a difference and I have personally posted 49 posts on my blog on different Tea Party heroes of mine.

What would happen if the debt ceiling was not increased? Yes President Obama would probably cancel White House tours and he would try to stop mail service or something else to get on our nerves but that is what the Republicans need to do.

I have written and emailed Senator Pryor over, and over again with spending cut suggestions but he has ignored all of these good ideas in favor of keeping the printing presses going as we plunge our future generations further in debt. I am convinced if he does not change his liberal voting record that he will no longer be our senator in 2014.

I have written hundreds of letters and emails to President Obama and I must say that I have been impressed that he has had the White House staff answer so many of my letters. The White House answered concerning Social Security (two times), Green Technologies, welfare, small businesses, Obamacare (twice), federal overspending, expanding unemployment benefits to 99 weeks, gun control, national debt, abortion, jumpstarting the economy, and various other issues. However, his policies have not changed, and by the way the White House after answering over 50 of my letters before November of 2012 has not answered one since. President Obama is committed to cutting nothing from the budget that I can tell.

I have praised over and over and over the 66 House Republicans that voted no on that before. If they did not raise the debt ceiling then we would have a balanced budget instantly. I agree that the Tea Party has made a difference and I have personally posted 49 posts on my blog on different Tea Party heroes of mine.

TRY BORROWING AT A BANK WITH A FINANCIAL CONDITION LIKE THE USA HAS:

The problem in Washington is not lack of revenue but our lack of spending restraint. This video below makes that point. WASHINGTON IS A SPENDING ADDICT!!!

Please take the time to read Mo Brooks’ words and respond to me and tell me if you will vote against the debt ceiling increase. It is the only leverage we have on President Obama. Others have responded to me in the past including you and for that I am very grateful.

Thank you for your time.

Sincerely,

Everette Hatcher, 13900 Cottontail Lane, Alexander, AR 72002, cell ph 501-920-5733, lowcostsqueegees@yahoo.com, www.thedailyhatch.org

_____________

Thank you so much for your time. I know how valuable it is. I also appreciate the fine family that you have and your commitment as a father and a husband.

Sincerely,

Everette Hatcher III, 13900 Cottontail Lane, Alexander, AR 72002, ph 501-920-5733, lowcostsqueegees@yahoo.com

Related posts:

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 49)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 49) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 48)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 48) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 47)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 47) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 46)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 46) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 45)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 45) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 44)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 44) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 43)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 43) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 42)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 42) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 41)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 41) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 40)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 40) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 39)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 39) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 38)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 38) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 37)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 37) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 36)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 36) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 35)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 35) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 34)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 34) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 33)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 33) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 32)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 32) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 31)

Congressmen Tim Huelskamp on the debt ceiling Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 31) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative […]

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 30)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 30) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 29)

Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 29) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, but […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 28)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 28) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 27)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 27) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 26)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 26) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 25)

Uploaded by RepJoeWalsh on Jun 14, 2011 Our country’s debt continues to grow — it’s eating away at the American Dream. We need to make real cuts now. We need Cut, Cap, and Balance. The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 25) This post today is a part of a series […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 23)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 23) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 22)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 22) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 21)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 21) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 20)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 20) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 19)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 19) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 18)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 18) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 17)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 17) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 16)

The Sixty Six who resisted “Sugar-coated Satan Sandwich” Debt Deal (Part 16) This post today is a part of a series I am doing on the 66 Republican Tea Party favorites that resisted eating the “Sugar-coated Satan Sandwich” Debt Deal. Actually that name did not originate from a representative who agrees with the Tea Party, […]

By Everette Hatcher III | Posted in spending out of control | Edit | Comments (0)