Why? Because I worry such terms imply a Trojan Horse for statism. And that’s definitely the case with so-called “stakeholder capitalism.”

As you can see, my core argument is that stakeholder capitalism is just another way of saying cronyism. And if I was being lazy, I would simply point out that Elizabeth Warren is a big proponent of the idea. That, by itself, should convince every thinking person that it’s a bad idea.

But I’m not going to be lazy. I’m going to cite some experts to show why stakeholder capitalism is bad news.

But first, I mentioned Milton Friedman’s famous quote in the above video clip.

Here’s the full quote, and notice that he explicitly says companies should follow rules – both legal and ethical – as they pursue profits.

Friedman was advocating what is sometimes referred to as “shareholder capitalism,” which is the notion that a company should strive to earn honest profits for its owners.

So what, then is stakeholder capitalism? In a columnfor the Wall Street Journal, Professor Alexander William Salter warns us that it is an invitation for intervention.

…beneath the lofty rhetoric, stakeholder capitalism is mostly a front for irresponsible corporatism. …Stakeholder capitalism is used as a way to obfuscate what counts as success in business. By focusing less on profits and more on vague social values, “enlightened” executives will find it easierto avoid accountability even as they squander business resources. While trying to make business about “social justice” is always concerning, the contemporary conjunction of stakeholder theory and woke capitalism makes for an especially dangerous and accountability-thwarting combination. …profits are an elegant and parsimonious way of promoting efficiency within a business as well as society at large. Stakeholder capitalism ruptures this process. When other goals compete with the mandate to maximize returns, the feedback loop created by profits gets weaker.

Writing for the Washington Post, George Will has a similarly scathing assessment.

…everyone who values economic dynamism, and the freedom that enables this, should recoil from the toxic noun “stakeholder.” …Stakeholder capitalism violates fiduciary laws that require those entrusted with investors’ money to employ it “solely in the interest of” and “for the exclusive purpose of providing benefits to” the investors. …In a dynamic society, resources are efficiently disposed by corporate managements whose primary duty, which other corporate activities do not compromise, is to maximize shareholder value… Self-proclaimed stakeholders, parasitic off others’ labor and accumulation, assert that everything is their business.

In a column for the Wall Street Journal, Phil Gramm and Mike Solon point out that today’s stakeholder capitalism is very similar to feudalism, which was a pre-industrial form of socialism.

…because of the misery Marxism has imposed, the world has a living memory and therefore some natural immunity to a system in which government takes the commanding heights of the economy. No such immunity exists to the older and therefore more dangerous socialism of the pre-Enlightenment world. In the communal world of the Dark Ages, the worker owed fealty to crown, church, guild and village. Those “stakeholders” extracted a share of the product of the sweat of the worker’s brow and the fruits of his thrift. …The 18th-century Enlightenment liberated…people to…own the fruits of their own labor and thrift. …These Enlightenment ideas spawned the Industrial Revolution and gave birth to the modern world… Remarkably, amid the recorded successes of capitalism and failures of socialism rooted in Marxism, pre-enlightenment socialism is re-emerging in the name of stakeholder capitalism. …the biggest losers in stakeholder capitalism are workers, whose wages will be cannibalized.

And the pursuit of profit is what generates efficiency, which is economic jargon for higher living standards. And that’s good for rich people and poor people.

The bottom line is that I’m not surprised when politicians support so-called stakeholder capitalism. After all, the crowd in Washington likes to have more power.

Based on what I said at the end of the above video, I’m disappointed – but not surprised – when big businesses (such as the Business Roundtable or Larry Fink of Blackrock) embrace the idea. After all, “creative destruction” is not so appealing when you’re already as the top.

This past article below from Dan Mitchell tells the story of Ronald Reagan’s successful strategy against inflation. I had a front row seat since I got to read the book and see the film FREE TO CHOOSE by Milton Friedman in 1980 who Reagan agreed with on this issue and I have included below the episode on inflation!

He also restored America’s national defenses and reoriented foreign policy, both of which led to the collapse of the Soviet Empire, a stupendous achievement that makes Reagan worthy of Mount Rushmore.

But he also has another great achievement, one that doesn’t receive nearly the level of appreciation that it deserves. President Reagan demolished the economic cancer of inflation.

Even Paul Krugman has acknowledged that reining in double-digit inflation was a major positive achievement. Because of his anti-Reagan bias, though, he wants to deny the Gipper any credit.

Robert Samuelson, in a column for the Washington Post, corrects the historical record.

Krugman recently wrote acolumnarguing that the decline of double-digit inflation in the 1980s was the decade’s big economic event, not the cuts in tax rates usually touted by conservatives. Actually, I agree with Krugman on this. But then he asserted that Ronald Reagan had almost nothing to do with it. That’s historically incorrect. Reagan was crucial. …Krugman’s error is so glaring.

Samuelson first provides the historical context.

For those too young to remember, here’s background. From 1960 to 1980, inflation — the general rise of retail prices —marched relentlessly upward. It went from 1.4 percent in 1960 to 5.9 percent in 1969 to 13.3 percent in 1979. The higher it rose, the more unpopular it became. …Worse, government seemed powerless to defeat it. Presidents deployed complex wage and price controls and guidelines. They didn’t work. The Federal Reserve — custodian of credit policies — veered between easy money and tight money, striving both to subdue inflation and to maintain “full employment” (taken as a 4 percent to 5 percent unemployment rate). It achieved neither. From the late 1960s to the early 1980s, there werefour recessions. Inflation became a monster, destabilizing the economy.

The column then explains that there was a dramatic turnaround in the early 1980s, as Fed Chairman Paul Volcker adopted a tight-money policy and inflation was squeezed out of the system much faster than almost anybody thought was possible.

But Krugman wants his readers to think that Reagan played no role in this dramatic and positive development.

Samuelson says this is nonsense. Vanquishing inflation would have been impossible without Reagan’s involvement.

What Reagan provided was political protection. The Fed’s previous failures to stifle inflation reflected its unwillingness to maintain tight-money policies long enough… Successive presidents preferred a different approach: the wage-price policies built on the pleasing (but unrealistic) premise that these could quell inflation without jeopardizing full employment. Reagan rejected this futile path. As the gruesome social costs of Volcker’s policies mounted — the monthly unemployment rate would ultimately rise to a post-World War II high of10.8 percent— Reagan’s approval ratings plunged. In May 1981, they were at 68 percent; by January 1983, 35 percent. Still, he supported the Fed. …It’s doubtful that any other plausible presidential candidate, Republican or Democrat, would have been so forbearing.

What’s the bottom line?

What Volcker and Reagan accomplished was an economic and political triumph. Economically, ending double-digit inflation set the stage for a quarter-century of near-automatic expansion… Politically, Reagan and Volcker showed that leaders can take actions that, though initially painful and unpopular, served the country’s long-term interests. …There was no explicit bargain between them. They had what I’ve called a “compact of conviction.”

By the way, Krugman then put forth a rather lame response to Samuelson, including the rather amazing claim that “[t]he 1980s were a triumph of Keynesian economics.”

As preached and practiced since the 1960s, Keynesian economics promised to stabilize the economy at levels of low inflation and high employment. By the early 1980s, this vision was in tatters, and many economists were fatalistic about controlling high inflation. Maybe it could be contained. It couldn’t be eliminated, because the social costs (high unemployment, lost output) would be too great. …This was a clever rationale for tolerating high inflation, and the Volcker-Reagan monetary onslaught demolished it. High inflation was not an intrinsic condition of wealthy democracies. It was the product of bad economic policies. This was the 1980s’ true lesson, not the contrived triumph of Keynesianism.

If anything, Samuelson is being too kind.

One of the key tenets of Keynesian economics is that there’s a tradeoff between inflation and unemployment (the so-called Phillips Curve).

Yet in the 1970s we had rising inflation and rising unemployment.

While in the 1980s, we had falling inflation and falling unemployment.

But if you’re Paul Krugman and you already have a very long list of mistakes (see here, here, here, here,here,here,here, here, andherefor a few examples), then why not go for the gold and try to give Keynes credit for the supply-side boom of the 1980s

P.S. Since today’s topic is Reagan, it’s a good opportunity to share my favorite poll of the past five years.

P.P.S. Here are some great videos of Reagan in action. And here’s one more if you need another Reagan fix.

Milton Friedman’s FREE TO CHOOSE “How to cure inflation” Transcript and Video (60 Minutes)

In 1980 I read the book FREE TO CHOOSE by Milton Friedman and it really enlightened me a tremendous amount. I suggest checking out these episodes and transcripts of Milton Friedman’s film series FREE TO CHOOSE: “The Failure of Socialism” and “What is wrong with our schools?” and “Created Equal” and From Cradle to Grave, and – Power of the Market.“If we could just stop the printing presses, we would stop inflation,” Milton Friedman says in “How to Cure Inflation” from the Free To Choose series. Now as then, there is only one cause of inflation, and that is when governments print too much money. Milton explains why it is that politicians like inflation, and why wage and price controls are not solutions to the problem.

http://www.freetochoosemedia.org/freetochoose/detail_ftc1980_transcript.php?page=9While many people have a fairly good grasp of what inflation is, few really understand its fundamental cause. There are many popular scapegoats: labor unions, big business, spendthrift consumers, greed, and international forces. Dr. Friedman explains that the actual cause is a government that has exclusive control of the money supply. Friedman says that the solution to inflation is well known among those who have the power to stop it: simply slow down the rate at which new money is printed. But government is one of the primary beneficiaries of inflation. By inflating the currency, tax revenues rise as families are pushed into higher income tax brackets. Thus, inflation transfers wealth and resources from the private to the public sector. In short, inflation is attractive to government because it is a way of increasing taxes without having to pass new legislation to raise tax rates. Inflation is in fact taxation without representation. Wage and price controls are not the cure for inflation because they treat only the symptom (rising prices) and not the disease (monetary expansion). History records that such controls do not work; instead, they have perverse effects on both prices and economic growth and undermine the fundamental productivity of the economy. There is only one cure for inflation: slow the printing presses. But the cure produces the painful side effects of a temporary increase in unemployment and reduced economic growth. It takes considerable political courage to undergo the cure. Friedman cites the example of Japan, which successfully underwent the cure in the mid-seventies but took five years to squeeze inflation out of the system. Inflation is a social disease that has the potential for destroying a free society if it is unchecked. Prolonged inflation undermines belief in the basic equity of the free market system because it tends to destroy the link between effort and reward. And it tears the social fabric because it divides society into winners and losers and sets group against group.(Taxation without representation: Getting knocked up to higher tax brackets because of inflation pt 1)http://www.youtube.com/watch?v=b1dTWDNKH3c

Volume 9 – How to Cure Inflation

Transcript:

Friedman: The Sierra Nevada’s in California 10,000 feet above sea level, in the winter temperatures drop to 40 below zero, in the summer the place bakes in the thin mountain air. In this unlikely spot the town of Body sprang up. In its day Body was filled with prostitutes, drunkards and gamblers part of a colorful history of the American West.

A century ago, this was a town of 10,000 people. What brought them here? Gold. If this were real gold, people would be scrambling for it. The series of gold strikes throughout the West brought people from all over the world, all kinds of people. They came here for one purpose and one purpose only, to strike it rich, quick. But in the process, they built towns, cities, in places where nobody would otherwise have dreamed of building a city. Gold built these cities and when the gold was exhausted, the cities collapsed and became ghost towns. Many of the people who came here ended up the way they began, broke and unhappy. But a few struck it rich. For them, gold was real wealth. But was it for the world as a whole. People couldn’t eat the gold, they couldn’t wear the gold, they couldn’t live in houses made of gold. Because there was more gold, they had to pay a little more gold to buy goods and services. The prices of things in terms of gold went up.

At tremendous cost, at sacrifice of lives, people dug gold out of the bowels of the earth. What happened to that gold? Eventually, at long last, it was transported to distant places only to be buried again under the ground. This time in the vaults of banks throughout the world. There is hardly anything that hasn’t been used for money; rock salt in Ethiopia, brass rings in West Africa, Calgary shells in Uganda, even a toy cannon. Anything can be used as money. Crocodile money in Malaysia, absurd isn’t it?

That beleaguered minority of the population that still smokes may recognize this stuff as the raw material from which their cigarettes are made. But in the early days of the colonies, long before the U.S. was established, this was money. It was the common money of Virginia, Maryland and the Carolinas. It was used for all sorts of things. The legislature voted that it could be used legally to pay taxes. It was used to buy food, clothing and housing. Indeed, one of the most interesting sites was to see the husky young fellows at that time, lug 100 pounds of it down to the docks to pay the costs of the passage of the beauteous young ladies who had come over from England to be their brides.

Now you know how money is. There’s a tendency for it to grow, for more and more of it to be produced and that’s what happened with this tobacco. As more tobacco was produced, there was more money. And as always when there’s more money, prices went up. Inflation. Indeed, at the very end of the process, prices were 40 times as high in terms of tobacco as they had been at the beginning of the process. And as always when inflation occurs, people complained. And as always, the legislature tried to do something. And as always, to very little avail. They prohibited certain classes of people from growing tobacco. They tried to reduce the total amount of tobacco grown, they required people to destroy part of their tobacco. But it did no good. Finally, many people took it into their own hands and they went around destroying other people’s tobacco fields. That was too much. Then they passed a law making it a capital offense, punishable by death, to destroy somebody else’s tobacco. Grecian’s Law, one of the oldest laws in economics, was well illustrated. That law says that cheap money drives out dear money and so it was with tobacco. Anybody who had a debt to pay, of course, tried to pay it in the worst quality of tobacco he had. He saved the good tobacco to sell overseas for hard money. The result was that bad money drove out good money.

Finally, almost a century after they had started using tobacco as money, they established warehouses in which tobacco was deposited in barrels, certified by an inspector according to his views as to it’s quality and quantity. And they issued warehouse certificates which people gave from one to another to pay for the bills that they accumulated.

These pieces of green printed paper are today’s counterparts of those tobacco certificates. Except that they bear no relation to any commodity. In this program I want to take you to Britain to see how inflation weakens the social fabric of society. Then to Tokyo, where the Japanese have the courage to cure inflation. To Berlin, where there is a lesson to be learned from the West Germans and how so called cures are often worse than the disease. And to Washington where our government keeps these machines working overtime. And I am going to show you how inflation can be cured.

The fact is that most people enjoy the early stages of the inflationary process. Britain, in the swinging 60’s, there was plenty of money around, business was brisk, jobs were plentiful and prices had not yet taken off. Everybody seemed happy at first. But by the early 70’s, as the good times rolled along, prices started to rise more and more rapidly. Soon, some of these people are going to lose their jobs. The party was coming to an end.

The story is much the same in the U.S. Only the process started a little later. We’ve had one inflationary party after another. Yet we still can’t seem to avoid them. How come?

Before every election our representatives would like to make us think we are getting a tax break. When they are able to do it, while at the same time actually raising our taxes because of a bit of magic they have in their kit bag. That magic is inflation. They reduced the tax rates but the taxes we have to pay go up because we are automatically shoved into higher brackets by the effective inflation. A neat trick. Taxation without representation.

_________________________________________

Pt 2 Many a political leader has been tempted to turn to wage and price controls despite their repeated failure in practice. On this subject they never seem to learn. But some lessons may be learned. That happened to British P

Bob Crawford: The more I work, it seems like the more they take off me. I know if I work an extra day or two extra days, what they take in federal income tax alone is almost doubled because apparently it puts you in a higher income tax bracket and it takes more off you.

Friedman: Bob Crawford lives with his wife and three children in a suburb of Pittsburgh. They’re a fairly average American family.

Mrs. Crawford: Don’t slam the door Daphne. Okay. Alright. What are you doing? Making your favorite dish.

Friedman: We went to the Crawford’s home after he had spent a couple of days working out his federal and state income taxes for the year. For our benefit, he tried to estimate all the other taxes he had paid as well. In the end, though, he didn’t discover much that would surprise anybody.

Bob Crawford: Inflation is going up, everything is getting more expensive. No matter what you do, as soon as you walk out of the house, everything went up. Your gas bills keep going up, electric bills, your gasoline, you can name a thousand things that are going up. Everything is going sky high. Your food. My wife goes to the grocery store. We used to live on say, $60 or $50 every two weeks just for our basic food. Now it’s $80 or $90 every two weeks. Things are just going out of sight as far as expense to live on. Like I say it’s getting tough. It seems like every month it gets worse and worse. And I don’t know where it’s going to end. At the end of the day that I spend nearly $6,000 of my earnings on taxes. That leaves me with a total of $12,000 to live on. It might seem like a lot of money, but five, six years ago I was earning $12,000.

Friedman: How does taxation without representation really effect how much the Crawford family has left to spend after it’s paid its income taxes. Well in 1972 Bob Crawford earned $12,000. Some of that income was not subject to income tax. After paying income tax on the rest he had this much left to spend. Six years later he was earning $18,000 a year. By 1978 the amount free from tax was larger. But he was now in a higher tax bracket so his taxes went up by a larger percentage than his income. However, those dollars weren’t worth anything like as much. Even his wages, let alone his income after taxes, hadn’t kept up with inflation. His buying power was lower than before. That is taxation without representation in practice.

Unnamed Individual: We have with us today you brothers that are sitting here today that were with us on that committee and I’d like to tell you….

Friedman: There are many traditional scapegoats blamed for inflation. How often have you heard inflation blamed on labor unions for pushing up wages. Workers, of course, don’t agree.

Unnamed Individual: But fellows this is not true. This is subterfuge. This is a myth. Your wage rates are not creating inflation.

Friedman: And he’s right. Higher wages are mostly a result of inflation rather than a cause of it. Indeed, the impression that unions cause inflation arises partly because union wages are slow to react to inflation and then there is pressure to catch up.

Worker: On a day to day basis, try to represent our own numbers. But that in fact is not the case. Not only can we not play catch up, we can’t even maintain a wage rate commensurate with the cost of living that’s gone up in this country.

Friedman: Another scapegoat for inflation is the cost of goods coming from abroad. Inflation, we’re told, is imported. Higher prices abroad driving up prices at home. It’s another way government can blame someone else for inflation. But this argument, too, is wrong. The prices of imports and the countries from which they come are not in terms of dollars, they are in terms of lira or yen or other foreign currencies. What happens to their prices in dollars depends on exchange rates which in turn reflect inflation in the United States.

Since 1973 some governments have had a field day blaming the Arabs for inflation. But if high oil prices were the cause of inflation, how is it that inflation has been less here in Germany, a country that must import every drop of oil and gas that it uses on the roads and in industry, then for example it is in the U.S. which produces half of its own oil. Japan has no oil of its own at all. Yet at the very time the Arabs were quadrupling oil prices, the Japanese people were bringing inflation down from 30 to less than 5% a year. The fallacy is to confuse particular prices like the price of oil, with prices in general. Back at home, President Nixon understood this.

Nixon: “Now here’s what I will not do. I will not take this nation down the road of wage and price controls however politically expedient that may seem. The pros of rationing may seem like an easy way out, but they are really an easy way in for more trouble. To the explosion that follows when you try to clamp a lid on a rising head of steam without turning down the fire under the pot, wage and price controls only postpone the day of reckoning. And in so doing, they rob every American of a very important part of his freedom.

Friedman: Now listen to this:

Nixon: “The time has come for decisive action. Action that will break the vicious circle of spiraling prices and costs. I am today ordering a freeze on all prices and wages throughout the United States for a period of 90 days. In addition, I call upon corporations to extend the wage price freeze to all dividends.”

Friedman: Many a political leader has been tempted to turn to wage and price controls despite their repeated failure in practice. On this subject they never seem to learn. But some lessons may be learned. That happened to British Prime Minister James Callahan who finally discovered that a very different economic myth was wrong. He told the Labor Party Conference about it in 1976.

James Callahan: “We used to think that you could use, spend your way out of a recession and increase employment by cutting taxes and boosting government spending. I tell you in all candor that option no longer exists. It only works on each occasion since the war by injecting a bigger dose of inflation into the economy followed by a higher level of unemployment as the next step. That’s the history of the last 20 years.”

Friedman: Well, it’s one thing to say it. One reason why inflation does so much harm is because it effects different groups differently. Some benefit and of course they attribute that to their own cleverness. Some are hurt, but of course they attribute that to the evil actions of other people. And the whole problem is made far worse by the false cures which government adopts, particularly wage and price control.

The garbage collectors in London felt justifiably aggrieved because their wages had not been permitted to keep pace with the cost of living. They struck, hurting not the people who impose the controls, but their friends and neighbors who had to live with mounting piles of rat infested garbage. Hospital attendants felt justifiably aggrieved because their wages had not been permitted to keep up with the cost of living. They struck, hurting not the people who impose the controls, but cancer patients who were turned out of hospital beds. The attendants behaved as a group in a way they never would have behaved as individuals. One group is set against another group. The social fabric of society is torn apart inflicting scars that it will take decades to heal and all to no avail because wage and price controls, far from being a cure for inflation, only make inflation worse.

Within the memory of most of our political leaders, there’s one vivid example of how economic ruin can be magnified by controls. And the classic demonstration of what to do when it happens.

_______________________________________________

(Wage and Price Controls don’t work)

Inflation is just like alcoholism. In both cases when you start drinking or when you start printing too much money, the good effects come first. The bad effects only come later.

That’s why in both cases there is a strong temptation to overdo it. To drink too much and to print too much money. When it comes to the cure, it’s the other way around. When you stop drinking or when you stop printing money, the bad effects come first and the good effects only come later.

Pt 3

Germany, 1945, a devastated country. A nation defeated in war. The new governing body was the Allied Control Commission, representing the United States, Britain, France and the Soviet Union. They imposed strict controls on practically every aspect of life including wages and prices. Along with the effects of war, the results were tragic. The basic economic order of the country began to collapse. Money lost its value. People reverted to primitive barter where they used cameras, fountain pens, cigarettes, whiskey as money. That was less than 40 years ago.

This is Germany as we know it today. Transformed into a place a lot of people would like to live in. How did they achieve their miraculous recovery? What did they know that we don’t know?

Early one Sunday morning, it was June 20, 1948, the German Minister of Economics, Ludwig Earhardt, a professional economist, simultaneously introduced a new currency, today’s Deutsche Mark, and in one fell swoop, abolished almost all controls on prices and wages. Why did he do it on a Sunday morning? It wasn’t as you might suppose because the Stock Markets were closed on that day, it was, as he loved to confess, because the offices of the American, the British, and the French occupation authorities were closed that day. He was sure that if he had done it when they open they would have countermanded the order. It worked like a charm. Within days, the shops were full of goods. Within months, the German economy was humming along at full steam. Economists weren’t surprised at the results, after all, that’s what a price system is for. But to the rest of the world it seemed an economic miracle that a defeated and devastated country could in little more than a decade become the strongest economy on the continent of Europe.

In a sense this city, West Berlin, is something of a unique economic test tube. Set as it is deep in Communist East Germany. Two fundamentally different economic systems collide here in Europe. Ours and theirs, separated by political philosophies, definitions of freedom and a steel and concrete wall.

To digress from inflation, economic freedom does not stand alone. It is part of a wider order. I wanted to show you how much difference it makes by letting you see how the people live on the other side of that Berlin Wall. But the East German authorities wouldn’t let us. The people over there speak the same language as the people over here. They have the same culture. They have the same for bearers. They are the same people. Yet you don’t need me to tell you how differently they live. There is one simple explanation. The political system over there cannot tolerate economic freedom. The political system over here could not exist without it.

But political freedom cannot be preserved unless inflation is kept in bounds. That’s the responsibility of government which has a monopoly over places like this. The reason we have inflation in the United States or for that matter anywhere in the world is because these pieces of paper and the accompanying book entry or their counterparts in other nations are growing more rapidly than the quantity of goods and services produced. The truth is inflation is made in one place and in one place only. Here in Washington. This is the only place were there are presses like this that turn out these pieces of paper we call money. This is the place where the power resides to determine how rapidly the amount of money shall increase.

What happened to all that noise? That’s what would happen to inflation if we stop letting the amount of money grow so rapidly. This is not a new idea. It’s not a new cure. It’s not a new problem. It’s happened over and over again in history. Sometimes inflation has been cured this way on purpose. Sometimes it’s happened by accident. During the Civil War the North, late in the Civil War, overran the place in the South where the printing presses were sitting up, where the pieces of paper were being turned out. Prior to that point, the South had a very rapid inflation. If my memory serves me right, something like 4% a month. It took the Confederacy something over two weeks to find a new place where they could set up their printing presses and start them going again. During that two week period, inflation came to a halt. After the two week period, when the presses started running again, inflation started up again. It’s that clear, that straightforward. More recently, there’s another dramatic example of the only effective way to deal with rampant inflation.

In 1973, Japanese housewives going to market were faced with an unpleasant fact. The cash in their purses seemed to be losing its value. Prices were starting to sore as the awful story of inflation began to unfold once again. The Japanese government knew what to do. What’s more, they were prepared to do it. When it was all over, economists were able to record precisely what had happened. In 1971 the quantity of money started to grow more rapidly. As always happens, inflation wasn’t affected for a time. But by late 1972 it started to respond. In early 73 the government reacted. It started to cut monetary growth. But inflation continued to soar for a time. The delayed reaction made 1973 a very tough year of recession. Inflation tumbled only when the government demonstrated its determination to keep monetary growth in check. It took five years to squeeze inflation out of the system. Japan attained relative stability. Unfortunately, there’s no way to avoid the difficult road the Japanese had to follow before they could have both low inflation and a healthy economy. First they had to live through a recession until slow monetary growth had its delayed effect on inflation.

Inflation is just like alcoholism. In both cases when you start drinking or when you start printing too much money, the good effects come first. The bad effects only come later.

That’s why in both cases there is a strong temptation to overdo it. To drink too much and to print too much money. When it comes to the cure, it’s the other way around. When you stop drinking or when you stop printing money, the bad effects come first and the good effects only come later. That’s why it’s so hard to persist with the cure. In the United States, four times in the 20 years after 1957, we undertook the cure. But each time we lacked the will to continue. As a result, we had all the bad effects and none of the good effects. Japan on the other hand, by sticking to a policy of slowing down the printing presses for five years, was by 1978 able to reap all the benefits, low inflation and a recovering economy. But there is nothing special about Japan. Every country that has had the courage to persist in a policy of slow monetary growth has been able to cure inflation and at the same time achieve a healthy economy.

___________________________________

Pt 4

The job of the Federal Reserve is not to run government spending; it’s not to run government taxation. The job of the Federal Reserve is to control the money supply and I believe, frankly, I have always believed as you know, that these are excuses and not reasons for the performance.

DISCUSSION

Participants: Robert McKenzie, Moderator; Milton Friedman; Congressman Clarence J. Brown; William M. Martin, Chairman of Federal Reserve 1951_1970; Beryl W. Sprinkel, Executive Vice President, Harris Bank, Chicago; Otmar Emminger, President, Ieutsche Bundesbank, Frankfurt West Germany

MCKENZIE: And here at the Harper Library of the University of Chicago, our distinguished guests have their own ideas, too. So, lets join them now.

BROWN: If you could control the money supply, you can certainly cut back or control the rate of inflation. I’d have to say that that prescription is a little bit easier to write than it is to fill. I think there are some other ways to do it and I would relate the money supply __ I think inflation is a measure of the relationship between money and the goods and services that money is meant to cover. And so if you can stimulate the goods, the production of goods and services, it’s helpful. It’s a little tougher to control the money supply, although I think it can be done, than just saying that you should control it, because we’ve got the growth of credit cards, which is a form of money; created, in effect, by the free enterprise system. It isn’t all just printed in Washington, but that may sound too defensive. I think he was right in saying that the inflation is Washington based.

MCKENZIE: Mr. Martin, nobody has been in the firing line longer than you, 17 years head of the Fed. Could you briefly comment on that and we’ll go around the group.

MARTIN: I want to say 19 years.

(Laughter)

MARTIN: I wouldn’t be out here if it weren’t for Milton Friedman, today. He came down and gave us advice from time to time.

FRIEDMAN: You’ve never taken it.

(Laughter)

MCKENZIE: He’s going to do some interviewing later, I warn you.

MARTIN: And I’m rather glad we didn’t take it __

(Laughter)

MARTIN: __ all the time.

SPRINKEL: In your 19 years as Chairman of the Federal Reserve, Bill, the average growth in the money supply was 3.1 percent per year. The inflation rate was 2.2 percent. Since you left, the money supply has exactly doubled. The inflation rate is average over 7 percent, and, of course, in recent times the money supply has been growing in double-digit territory as has our inflation rate.

EMMINGER: May I, first of all, confirm two facts which have been so vividly brought out in the film of Professor Friedman; namely, that at the basis of the relatively good performance of Western Germany were really two events. One, the establishment of a new sound money which we try to preserve sound afterwards. And, secondly, the jump overnight into a free market economy without any controls over prices and wages. These are the two fundamental facts. We have tried to preserve monetary stability by just trying to follow this prescription of Professor Friedman; namely, monetary discipline. Keeping monetary growth relatively moderate. I must, however, warn you it’s not so easy as it looks. If you just say, governments have to have the courage to persist in that course.

FRIEDMAN: Nobody does disagree with the proposition that excessive growth in money supply is an essential element in the inflationary process and that the real problem is not what to do, but how to have the courage and the will to do it. And I want to go and start, if I may, on that subject; because I think that’s what we ought to explore. Why is it we haven’t had the courage and don’t, and under what circumstances will we? And I want to start with Bill Martin because his experience is a very interesting experience. His 19 years was divided into different periods. In the first period, that average that Beryl Sprinkel spoke about, averaged two very different periods. An early period of very slow growth and slow inflation; a later period of what at the time was regarded as creeping inflation __ now we’d be delighted to get back to it. People don’t remember that at the time that Mr. Nixon introduced price and wage controls in 1971 to control an outrageous inflation, the rate of inflation was four-and-a-half percent per year. Today we’d regard that as a major achievement; but the part of the period when you were Chairman, was a period when the inflation rate was starting to creep up and money growth rate was also creeping up. Now if I go from your period, you were eloquent in your statements to the public, to the press, to everyone, about the evils of inflation, and about the determination on the Federal Reserve not to be the architect of inflation. Your successor, Arthur Burns, was just as eloquent. Made exactly the same kinds of statements as effectively, and again over and over again said the Federal Reserve will not be the architect of inflation. His successor, Mr. G. William Miller, made the same speeches, and the same statements, and the same protestations. His successor, Paul Volcker, he is making the same statements. Now my question to you is: Why is it that there has been such a striking difference between the excellent pronouncements of all Chairmen of the Fed, therefore it’s not personal on you. You have a lot of company, unfortunately for the country. Why is it that there has been such a wide diversion between the excellent pronouncements on the one hand and what I regard as a very poor performance on the other?

MARTIN: Because monetary policy is not the only element. Fiscal policy is equally important.

FRIEDMAN: You’re shifting the buck to the Treasury.

MARTIN: Yes.

FRIEDMAN: To the Congress. We’ll get to Mr. Brown, don’t worry.

MARTIN: Yeah, that’s right.

(Laughter)

MARTIN: The relationship of fiscal policy to monetary policy is one of the important things.

MCKENZIE: Would you remind us, the general audience, when you say “fiscal policy”, what you mean in distinction to “monetary policy”?

MARTIN: Well, taxation.

MCKENZIE: Yeah.

MARTIN: The raising revenue.

FRIEDMAN: And spending.

MARTIN: And spending.

FRIEDMAN: And deficits.

MARTIN: And deficits, yes, exactly. And I think that you have to realize that when I’ve talked for a long time about the independence of the Federal Reserve. That’s independence within the government, not independence of the government. And I’ve worked consistently with the Treasury to try to see that the government is financed. Now this gets back to spending. The government says they’re gonna spend a certain amount, and then it turns out they don’t spend that amount. It doubles.

FRIEDMAN: The job of the Federal Reserve is not to run government spending; it’s not to run government taxation. The job of the Federal Reserve is to control the money supply and I believe, frankly, I have always believed as you know, that these are excuses and not reasons for the performance.

MARTIN: Well that’s where you and I differ, because I think we would be irresponsible if we didn’t take into account the needs and what the government is saying and doing. I think if we just went on our own, irresponsibly, I say it on this, because I was in the Treasury before I came to this __

FRIEDMAN: I know. I know.

MARTIN: __ go to the Fed; and I know the other side of the picture. I think we’d be rightly condemned by the American people and by the electorate.

FRIEDMAN: Every central bank in this world, including the German Central Bank, including the Federal Reserve System, has the technical capacity to make the money supply do over a period of two or three or four months, not daily, but over a period, has the technical capacity to control it.

(Several people talking at once.)

FRIEDMAN: I cannot explain the kind of excessive money creation that has occurred, in terms of the technical incapacity of the Federal Reserve System or of the German Central Bank, or of the Bank of England, or any other central bank in the world.

EMMINGER: I wouldn’t say technically we are incapable of doing that, although we have never succeeded in controlling the money supply month that way. But I would say we can, technically, control it half yearly, from one half-year period to the next and that would be sufficient __

FRIEDMAN: That would be sufficient.

EMMINGER: __ for controlling inflation. But however I __

VOICE OFF SCREEN: It doesn’t move.

FRIEDMAN: I’m an economic scientist, and I’m trying to observe phenomena, and I observe that every Federal Reserve Chairman says one thing and does another. I don’t mean he does, the system does.

MCKENZIE: Yeah. How different is your setup in Germany? You’ve heard this problem of governments getting committed to spending and the Fed having, one way or the other, to accommodate itself to it. Now what’s your position on this very interesting problem?

EMMINGER: We are very independent of the government, from the government, but, on the other hand, we are an advisor of the government. Also on the budget deficits and they would not easily go before Parliament with a deficit which much of it is openly criticized and disapproved by the same bank. Why because we have a tradition in our country that we can also publicly criticize the government on his account. And second, as if happened in our case too, the government goes beyond what is tolerable for the sake of moral equilibrium. We have let it come through in the capital markets. That is to say they have enough interest rates that has drawn public criticism and that has had some effect on their attitude.

_________________________________________

Pt 5

I think that is a very important point that Dr. Emminger just made because there is not a one-to-one relationship between government deficits and what happens to the money supply at all. The pressure on the Federal Reserve comes indirectly. It comes because large government deficits, if they are financed in the general capital market, will drive up interest rates and then we have the right patents in Congress and their successors pressuring the Federal Reserve to enter in and finance the deficit by printing money as a way of supposedly holding down interest rates. Now before I turn to Mr. Brown and ask him that, I just want to make one point which is very important. The Federal Reserve’s activities in trying to hold down interest rates have put us in a position where we have the highest interest rates in history. It’s another example of how, of the difference between the announced intentions of a policy, and the actual results. But now I want to come to Clarence Brown and ask him, shift the buck to him, and put him on the hot seat for a bit. The government spending has been going up rapidly, Republican administration or Democratic administration. This is a nonpartisan issue, it doesn’t matter. Government deficits have been going up rapidly. Republican administration or Democratic administration. Why is it that here again you have the difference between pronouncements and performance? There is no Congressman, no Senator, who will come out and say, “I am in favor of inflation.” There is not a single one who will say, “I am in favor of big deficits.” They’ll all say we want to balance the budget, we want to hold down spending, we want an economical government. How do you explain the difference between performance and talk on the side of Congress?

BROWN:

FRIEDMAN: I think that is a very important point that Dr. Emminger just made because there is not a one-to-one relationship between government deficits and what happens to the money supply at all. The pressure on the Federal Reserve comes indirectly. It comes because large government deficits, if they are financed in the general capital market, will drive up interest rates and then we have the right patents in Congress and their successors pressuring the Federal Reserve to enter in and finance the deficit by printing money as a way of supposedly holding down interest rates. Now before I turn to Mr. Brown and ask him that, I just want to make one point which is very important. The Federal Reserve’s activities in trying to hold down interest rates have put us in a position where we have the highest interest rates in history. It’s another example of how, of the difference between the announced intentions of a policy, and the actual results. But now I want to come to Clarence Brown and ask him, shift the buck to him, and put him on the hot seat for a bit. The government spending has been going up rapidly, Republican administration or Democratic administration. This is a nonpartisan issue, it doesn’t matter. Government deficits have been going up rapidly. Republican administration or Democratic administration. Why is it that here again you have the difference between pronouncements and performance? There is no Congressman, no Senator, who will come out and say, “I am in favor of inflation.” There is not a single one who will say, “I am in favor of big deficits.” They’ll all say we want to balance the budget, we want to hold down spending, we want an economical government. How do you explain the difference between performance and talk on the side of Congress?

BROWN: Well, first I think we have to make one point. I’m not so much with the government as I am against it.

FRIEDMAN: I understand.

BROWN: As you know, I’m a minority member of Congress.

FRIEDMAN: Again, I’m not __ I’m not directing this at you personally.

BROWN: I understand, of course; and while the administrations, as you’ve mentioned, Republican and Democratic administrations, have both been responsible for increases in spending, at least in terms of their recommendations. It is the Congress and only the Congress that appropriates the funds and determines what the taxes are. The President has no authority to do that and so one must lay it at the feet of the U.S. Congress. Now, I guess we’d have to concede that it’s a little bit more fun to give away things than it is to withhold them. And this is the reason that the Congress responds to a general public that says, “I want you to cut everybody else’s program but the one in which I am most particularly interested. Save money, but incidentally, my wife is taking care of the orphanages and so lets try to help the orphanages,” or whatever it is. Let me try to make a point, if I can, however, on what I think is a new spirit moving within the Congress and that is that inflation, as a national affliction, is beginning to have an impact on the political psychology of many Americans. Now the Germans, the Japanese and others have had this terrific postwar inflation. The Germans have been through it twice, after World War I and World War II, and it’s a part of their national psyche. But we are affected in this country by the depression. Our whole tax structure is built on the depression. The idea of the tax structure in the past has been to get the money out of the mattress where it went after the banks failed in this country and jobs were lost, and out of the woodshed or the tin box in the back yard, get it out of there and put it into circulation. Get it moving, get things going. And one of the ways to do that was to encourage inflation. Because if you held on to it, the money would depreciate; and the other way was to tax it away from people and let the government spend it. Now there’s a reaction to that and people are beginning to say, “Wait just a minute. We’re not afflicted as much as we were by depression. We’re now afflicted by inflation, and we’d like for you to get it under control.” Now you can do that in another way and that without reducing the money supply radically. I think the Joint Economic Committee has recommended that we do it gradually. But the way that you can do it is to reduce taxes and the impact of government, that is the weight of government and increase private savings so that the private savings can finance some of the debt that you have.

FRIEDMAN: There is no way you can do it without reducing, in my opinion, the rate of monetary growth. And I, recognizing the facts, even though they ought not to be that way, I wonder whether you can reduce the rate of monetary growth unless Congress actually does reduce government spending as well as government taxes.

BROWN: The problem is that every time we use demand management, we get into a kind of an iron maiden kind of situation. We twist this way and one of the spikes grabs us here, so we twist that way and a spike over here gets us. And every recession has had higher basic unemployment rates than the previous recession in the last several years and every inflation has had higher inflation. We’ve got to get that tilt out of the society.

MCKENZIE: Wouldn’t it be fair to say, though, that a fundamental difference is the Germans are more deeply fearful of a return to inflation, having had the horrifying experience between the wars, especially. We tend to be more afraid of recession turning into depression.

EMMINGER: I think there is something in it and in particular in Germany the government would have to fear very much in their electoral prospects if they went into such an election period with a high inflation rate. But there is another important difference.

MARTIN: We fear unemployment more than inflation it seems.

EMMINGER: You fear unemployment, but unemployment is feared with us, too, but inflation is just as much feared. But there is another difference; namely, once you have got into that escalating inflation, every time the base, the plateau is higher, it’s extremely difficult to get out of it. You must avoid getting into that, now that’s very cheap advice from me because you are now.

(Laughing)

EMMINGER: But we had, for the last fifteen, twenty years, always studied foreign experiences, and told ourselves we never must get into this vicious circle. Once you are in, it takes a long time to get out of it. That is what I am preaching now, that we should avoid at all costs to get again into this vicious circle as we had it already in ’73_’74. It took us, also, four years to get out of it, although we were only at eight percent inflation. Four years to get down to three percent. So you __

MCKENZIE: Those were __ yes.

EMMINGER: You have, I think, the question of whether you can do if in a gradualist way over many, many years, or whether you don’t need a sort of shock treatment.

____________________________________

her we go into a period of still higher unemployment later on and have it to do all over again. That’s the only choice we face. And when the public at large recognizes that, they will then elect people to Congress, and a President to office who is committed to less government spending and to less government printing of money and until that happens we will not cure inflation

Pt 6

SPRINKEL: The film said it took the Japanese _ what _ four years?

FRIEDMAN: Five years.

SPRINKEL: Five years. But one of my greatest concerns is that we haven’t suffered enough yet. Most of the nations that have finally got their inflations __

BROWN: Bad election speech.

SPRINKEL: __ well, I’m not running for office, Clarence.

(Laughter)

SPRINKEL: Most countries that finally got their inflation under control had 20, 30 percent or worse inflation. Germany had much worse and the public supports them. We live in a Democracy, and we’re getting constituencies that gain from inflation. You look at people that own real estate, they’ve done very well.

MCKENZIE: Yes.

SPRINKEL: And how can we get there without going through even more pain, and I doubt that we will.

FRIEDMAN: If you ask who are the constituencies that have benefited most from inflation there are no doubt, it is the homeowners.

SPRINKEL: Yes.

FRIEDMAN: But it’s also the __ it’s also the Congressmen who have been able to vote higher spending without having to vote higher taxes. They have in fact __

BROWN: That’s right.

FRIEDMAN: __ Congress has in fact voted for inflation. But you have never had a Congressman on record to that effect. It’s the government civil servants who have their own salaries are indexed and tied to inflation. They have a retirement benefit, a retirement pension that’s tied to inflation. They qualify, a large fraction of them, for Social Security as well, which is tied to inflation. So that the beneficial __

BROWN: Labor contracts that are indexed and many pricing things that are tied to it.

FRIEDMAN: But the one thing that isn’t tied to inflation and here I want to come back and ask why Congress has been so __ so bad in this area, is our taxes. It has been impossible to get Congress to index the tax system so that you don’t have the present effect where every one percent increase in inflation pushes people up into higher brackets and forces them to pay higher taxes.

BROWN: Well, as you know, I’m an advocate of that.

FRIEDMAN: I know you are.

MCKENZIE: Some countries do that, of course.

FRIEDMAN: Oh, of course.

MCKENZIE: Canada does that. Indexes the __

BROWN: And I went up to Canada on a little weekend seminar program on indexing and came back an advocate of indexing because I found out that the people who are delighted with indexing are the taxpayers.

FRIEDMAN: Absolutely.

BROWN: Because as the inflation rate goes up their tax level either maintains at the same level or goes down. The people who are least __ well, the people who are very unhappy with it are the people who have to plan government spending because it is reducing the amount of money that the government has rather than watching it go up by ten or twelve billion. You get a little dividend to spend in this country, the bureaucrats do every year, but the politicians are unhappy with it too, as Dr. Friedman points out because, you see, politicians don’t get to vote a tax reduction, it happens automatically.

MCKENZIE: Yeah.

BROWN: And so you can’t go back and in a praiseworthy way tell your constituents that I am for you, I voted a tax reduction. And I think we ought to be able to index the tax system so that tax reduction is automatic, rather than have what we’ve had in the past, and that is an automatic increase in the taxes. And the politicians say, “Well, we’re sorry about inflation, but __”.

FRIEDMAN: You’re right and I want to __ I want to go and make a very different point. I sit here and berate you and you as government officials, and so on, but I understand very well that the real culprits are not the politicians, are not the central bankers, but it’s I and my fellow citizens. I always say to people when I talk about this, “If you want to know who’s responsible for inflation, look in the mirror.” It’s not because of the way you spend you money. Inflation doesn’t arise because you got consumers who are spendthrifts; they’ve always been spendthrifts. It doesn’t arise because you’ve got businessmen who are greedy. They’ve always been greedy. Inflation arises because we as citizens have been asking you as politicians to perform an impossible task. We’ve been asking you to spend somebody else’s money on us, but not to spend our money on anybody else.

BROWN: You don’t want us to cut back those dollars for education, right?

FRIEDMAN: Right. And, therefore, __ well, no, I do.

MCKENZIE: We’ve already had a program on that.

FRIEDMAN: We’ve already had a program on that and there’s no viewer of these programs who will be in any doubt about my position on that. But the public at large has not and this is where we come to the political will that Dr. Emminger quite properly talked about. It is __ everybody talks against inflation, but what he means is that he wants the prices of the things he sells to go up and the prices of the things he buys to go down. But, sooner or later, we come to the point where it will be politically profitable to end inflation. This is the point that __

SPRINKEL: Yes.

FRIEDMAN: __ I think you were making.

SPRINKEL: The suffering idea.

FRIEDMAN: Where do you think the __ you know, what do you think the rate of inflation has to be and judged by the experience of other countries before we will be in that position and when do you think that will happen?

SPRINKEL: Well, the evidence says it’s got to be over 20 percent. Now you would think we could learn from others rather than have to repeat mistakes.

FRIEDMAN: Apparently nobody can learn from history.

SPRINKEL: But at the present time we’re going toward higher and not lower inflation.

MCKENZIE: You said earlier, if you want to see who causes inflation look in the mirror.

FRIEDMAN: Right.

MCKENZIE: Now, for everybody watching and taking part in this, there must be some moral to that. What does need __ what has to be the change of attitude of the man in the mirror you’re looking at before we can effectively implement what you call a tough policy that takes courage?

FRIEDMAN: I think that the man in the mirror has to come to recognize that inflation is the most destructive disease known to modern society. There is nothing which will destroy a society so thoroughly and so fully as letting inflation run riot. He must come to recognize that he doesn’t have any good choices. That there are no easy answers. That once you get in this situation where the economy is sick of this insidious disease, there’s gonna be no miracle drug which will enable them to be well tomorrow. That the only choices he has, do I go through a tough period for four or five years of relatively high unemployment, relatively low growth or do I try to push it off by taking some more of the hair of the dog that bit me and get around it now at the cost of still higher unemployment, as Clarence Brown said, later on. The only choice this country faces, is whether we have temporary unemployment for a short period, as a side effect of curling inflation or whether we go into a period of still higher unemployment later on and have it to do all over again. That’s the only choice we face. And when the public at large recognizes that, they will then elect people to Congress, and a President to office who is committed to less government spending and to less government printing of money and until that happens we will not cure inflation.

____________________________________

FRIEDMAN: And therefore the crucial thing is to cut down total government spending from the point of view of inflation. From the point of view of productivity, some of the other measures you were talking about are far more important.

BROWN

Pt 7

BROWN: But, Dr. Friedman, let me __

(Applause)

BROWN: Let me differ with you to this extent. I think it is important that at the time you are trying to get inflation out of the economy that you also give the man in the street, the common man, the opportunity to have a little bit more of his own resources to spend. And if you can reduce his taxes at that time and then reduce government in that process, you give him his money to spend rather than having to yield up all that money to government. If you cut his taxes in a way to encourage it, to putting that money into savings, you can encourage the additional savings in a private sense to finance the debt that you have to carry, and you can also encourage the stimulation of growth in the society, that is the investment into the capital improvements of modernization of plant, make the U.S. more competitive with other countries. And we can try to do it without as much painful unemployment as we can get by with. Don’t you think that has some merit?

FRIEDMAN: The only way __ I am all in favor, as you know, of cutting government spending. I am all in favor of getting rid of the counterproductive government regulation that reduces productivity and disrupts investment. But __

BROWN: And we do that, we can cut taxes some, can we not?

FRIEDMAN: We should __ taxes __ but you are introducing a confusion that has confused the American people. And that is the confusion between spending and taxes. The real tax on the American people is not what you label taxes. It’s total spending. If Congress spends fifty billion dollars more than it takes in, if government spends fifty billion dollars, who do you suppose pays that fifty billion dollars?

BROWN: Of course, of course.

FRIEDMAN: The Arab Sheiks aren’t paying it. Santa Claus isn’t paying it. The Tooth Fairy isn’t paying it. You and I as taxpayers are paying it indirectly through hidden taxation.

MCKENZIE: Your view __

FRIEDMAN: And therefore the crucial thing is to cut down total government spending from the point of view of inflation. From the point of view of productivity, some of the other measures you were talking about are far more important.

BROWN: But if you concede that inflation and taxes are both part and parcel of the same thing, and if you cut spending __

FRIEDMAN: They’re not part and parcel of the same thing.

BROWN: If you cut spending you __ well, but, you take the money from them in one way or another. The average citizen.

FRIEDMAN: Absolutely.

BROWN: To finance the growth of government.

FRIEDMAN: That’s right.

BROWN: So if you cut back the size of government, you can cut both their inflation and their taxes.

FRIEDMAN: That’s right.

BROWN: If you __

FRIEDMAN: I am all in favor of that.

BROWN: All right.

FRIEDMAN: All I am saying is don’t kid yourself into thinking that there is some painless way to do it. There just is not.

BROWN: One other way is productivity. If you can __ if you can increase production, then the impact of inflation is less because you have more goods chasing __

FRIEDMAN: Absolutely, but you have to have a sense of proportion. From the point of view of the real income of the American people, nothing is more important than increasing productivity. But from the point of view of inflation, it’s a bit actor. It would be a miracle if we could raise our productivity from three to five percent a year, that would reduce inflation by two percent.

BROWN: No question, it won’t happen overnight, but it’s part of the __ it’s part of a long range squeezing out of inflation.

FRIEDMAN: There is only one way to ease the __ in my opinion there is only one way to ease the pains of curing inflation and that way is not available. That way is to make it credible to the American people that you are really going to follow the policy you say you’re going to follow. Unfortunately I don’t see any way we can do that.

(Several people talking at once.)

EMMINGER: Professor Friedman, that’s exactly the point which I wanted to illustrate by our own experience. We also had to squeeze out inflation and there was a painful time of one-and-a-half years, but after that we had a continuous lowering of the inflation rate with a slow upward movement in the economy since 1975. Year by year inflation went down and we had a moderate growth rate which has led us now to full employment.

FRIEDMAN: That’s what __

EMMINGER: So you can shorten this period by just this credibility and by a consensus you must have, also with the trade unions, with the whole population that they acknowledge that policy and also play their part in it. Then the pains will be much less.

SPRINKEL: You see in our case, expectations are that inflation’s going to get worse because it always has. This means we must disappoint in a very painful way those expectations and it’s likely to take longer, at least the first time around. Now our real problem has not been that we haven’t tried. We have tried and brought inflation down. Our real problem was, we didn’t stick to it. And then you have it all to do over.

BROWN: Well I would __ I would concede that psychology plays a great, perhaps even the major part, but I do believe that if you have private savings stimulated by your tax system, rather than discouraged by your tax system, you can finance some of that public debt by private savings rather than by inflation and the result will be to ease to some degree the paint of that heavy unemployment that you seem to suggest is the only way to deal with the problem.

FRIEDMAN: The talk is fine, but the problem is that it’s used to evade the key issue: How do you make it credible to the public that you are really going to stick to a policy? Four times we’ve tried it and four times we’ve stopped before we’ve run the course.

(Several people talking at once.)

MCKENZIE: There we leave the matter for tonight, and next week’s concluding program in this series is not to be missed.

Milton Friedman The Power of the Market 1-5 How can we have personal freedom without economic freedom? That is why I don’t understand why socialists who value individual freedoms want to take away our economic freedoms. I wanted to share this info below with you from Milton Friedman who has influenced me greatly over the […]

Milton Friedman: Free To Choose – The Failure Of Socialism With Ronald Reagan (Full) Published on Mar 19, 2012 by NoNationalityNeeded Milton Friedman’s writings affected me greatly when I first discovered them and I wanted to share with you. We must not head down the path of socialism like Greece has done. Abstract: Ronald Reagan […]

Worse still, America’s depression was to become worldwide because of what lies behind these doors. This is the vault of the Federal Reserve Bank of New York. Inside is the largest horde of gold in the world. Because the world was on a gold standard in 1929, these vaults, where the U.S. gold was stored, […]

George Eccles: Well, then we called all our employees together. And we told them to be at the bank at their place at 8:00 a.m. and just act as if nothing was happening, just have a smile on their face, if they could, and me too. And we have four savings windows and we […]

Milton Friedman’s Free to Choose (1980), episode 3 – Anatomy of a Crisis. part 1 FREE TO CHOOSE: Anatomy of Crisis Friedman Delancy Street in New York’s lower east side, hardly one of the city’s best known sites, yet what happened in this street nearly 50 years ago continues to effect all of us today. […]

Friedman Friday” Free to Choose by Milton Friedman: Episode “What is wrong with our schools?” (Part 3 of transcript and video) Here is the video clip and transcript of the film series FREE TO CHOOSE episode “What is wrong with our schools?” Part 3 of 6. Volume 6 – What’s Wrong with our Schools Transcript: If it […]

Here is the video clip and transcript of the film series FREE TO CHOOSE episode “What is wrong with our schools?” Part 2 of 6. Volume 6 – What’s Wrong with our Schools Transcript: Groups of concerned parents and teachers decided to do something about it. They used private funds to take over empty stores and they […]

Here is the video clip and transcript of the film series FREE TO CHOOSE episode “What is wrong with our schools?” Part 1 of 6. Volume 6 – What’s Wrong with our Schools Transcript: Friedman: These youngsters are beginning another day at one of America’s public schools, Hyde Park High School in Boston. What happens when […]

Friedman Friday” Free to Choose by Milton Friedman: Episode “Created Equal” (Part 3 of transcript and video) Liberals like President Obama want to shoot for an equality of outcome. That system does not work. In fact, our free society allows for the closest gap between the wealthy and the poor. Unlike other countries where free enterprise and other […]

Free to Choose by Milton Friedman: Episode “Created Equal” (Part 2 of transcript and video) Liberals like President Obama want to shoot for an equality of outcome. That system does not work. In fact, our free society allows for the closest gap between the wealthy and the poor. Unlike other countries where free enterprise and other freedoms are […]

Milton Friedman and Ronald Reagan Liberals like President Obama (and John Brummett) want to shoot for an equality of outcome. That system does not work. In fact, our free society allows for the closest gap between the wealthy and the poor. Unlike other countries where free enterprise and other freedoms are not present. This is a seven part series. […]

I am currently going through his film series “Free to Choose” which is one the most powerful film series I have ever seen. PART 3 OF 7 Worse still, America’s depression was to become worldwide because of what lies behind these doors. This is the vault of the Federal Reserve Bank of New York. Inside […]

I am currently going through his film series “Free to Choose” which is one the most powerful film series I have ever seen. For the past 7 years Maureen Ramsey has had to buy food and clothes for her family out of a government handout. For the whole of that time, her husband, Steve, hasn’t […]

Friedman Friday:(“Free to Choose” episode 4 – From Cradle to Grave, Part 1 of 7) Volume 4 – From Cradle to Grave Abstract: Since the Depression years of the 1930s, there has been almost continuous expansion of governmental efforts to provide for people’s welfare. First, there was a tremendous expansion of public works. The Social Security Act […]

_________________________ Pt3 Nowadays there’s a considerable amount of traffic at this border. People cross a little more freely than they use to. Many people from Hong Kong trade in China and the market has helped bring the two countries closer together, but the barriers between them are still very real. On this side […]

Aside from its harbor, the only other important resource of Hong Kong is people __ over 4_ million of them. Like America a century ago, Hong Kong in the past few decades has been a haven for people who sought the freedom to make the most of their own abilities. Many of them are […]

“FREE TO CHOOSE” 1: The Power of the Market (Milton Friedman) Free to Choose ^ | 1980 | Milton Friedman Posted on Monday, July 17, 2006 4:20:46 PM by Choose Ye This Day FREE TO CHOOSE: The Power of the Market Friedman: Once all of this was a swamp, covered with forest. The Canarce Indians […]

Milton Friedman: Free To Choose – The Failure Of Socialism With Ronald Reagan (Full) Published on Mar 19, 2012 by NoNationalityNeeded Milton Friedman’s writings affected me greatly when I first discovered them and I wanted to share with you. We must not head down the path of socialism like Greece has done. Abstract: Ronald Reagan […]

I have an old-fashioned belief that it’s important to be truthful when analyzing public policy. I criticize Republicans when they’re wrong and I criticize Democrats when they’re wrong. And I also praise politicians from bothparties in those rare moments when they do good things.

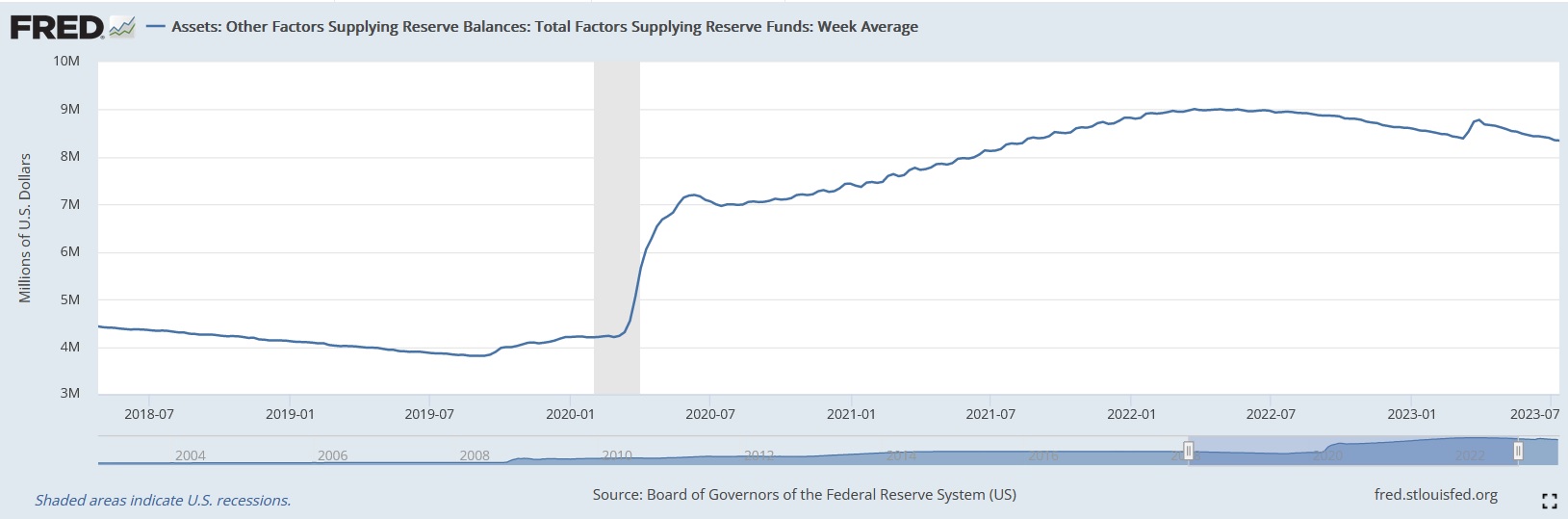

I explained that the Federal Reserve was the culprit. America’s central bank panicked during the pandemic and dramatically increased its balance sheet. In simpler terms, they created a huge amount of new money in the economy.

And they continued with that flawed policy even after it became apparent the world wasn’t coming to an end.

The good news is that inflation is now coming down. Catherine Rampell of the Washington Post wants Joe Biden to get the credit. But she explains that he deserves credit for something he didn’t do rather than any of his policies. Here are some excerpts from her column.

…what do Democrats say is moderating price growth…? The White House credits “Bidenomics.” What that means is unclear; administration officials tout vague platitudes about “building the economy from the middle out and bottom up,” as well asbig, recently passed industrial policies… But if you instead define Bidenomics as “respecting Federal Reserve independence and not interfering with Fed decisions even when they’re unpopular,” then sure: Great job, Bidenomics! …The president has been terrific at staying out of the Fed’s way, something presidents don’t always do.

I don’t always agree with Ms. Rampell, but I think this analysis is correct.

The Fed made a mess with bad monetary policy and only the Fed can fix that mistake. Biden, as Rampell noted, “has been terrific at staying out of the Fed’s way.”

If you want to understand the economics of why inflation is beginning to abate, this chart from the St. Louis Federal Reserve provides the answer. Simply stated, the Fed finally has started to withdraw some of the excess money it dumped into the economy.

By the way, while the Fed is finally doing the right thing, the central bank does not deserve praise. The nation could have avoided the pain of inflation if the Fed hadn’t started the boom-bust cycle in the first place.

This past article below from Dan Mitchell tells the story of Ronald Reagan’s successful strategy against inflation. I had a front row seat since I got to read the book and see the film FREE TO CHOOSE by Milton Friedman in 1980 who Reagan agreed with on this issue and I have included below the episode on inflation!

He also restored America’s national defenses and reoriented foreign policy, both of which led to the collapse of the Soviet Empire, a stupendous achievement that makes Reagan worthy of Mount Rushmore.

But he also has another great achievement, one that doesn’t receive nearly the level of appreciation that it deserves. President Reagan demolished the economic cancer of inflation.

Even Paul Krugman has acknowledged that reining in double-digit inflation was a major positive achievement. Because of his anti-Reagan bias, though, he wants to deny the Gipper any credit.

Robert Samuelson, in a column for the Washington Post, corrects the historical record.

Krugman recently wrote acolumnarguing that the decline of double-digit inflation in the 1980s was the decade’s big economic event, not the cuts in tax rates usually touted by conservatives. Actually, I agree with Krugman on this. But then he asserted that Ronald Reagan had almost nothing to do with it. That’s historically incorrect. Reagan was crucial. …Krugman’s error is so glaring.

Samuelson first provides the historical context.

For those too young to remember, here’s background. From 1960 to 1980, inflation — the general rise of retail prices —marched relentlessly upward. It went from 1.4 percent in 1960 to 5.9 percent in 1969 to 13.3 percent in 1979. The higher it rose, the more unpopular it became. …Worse, government seemed powerless to defeat it. Presidents deployed complex wage and price controls and guidelines. They didn’t work. The Federal Reserve — custodian of credit policies — veered between easy money and tight money, striving both to subdue inflation and to maintain “full employment” (taken as a 4 percent to 5 percent unemployment rate). It achieved neither. From the late 1960s to the early 1980s, there werefour recessions. Inflation became a monster, destabilizing the economy.

The column then explains that there was a dramatic turnaround in the early 1980s, as Fed Chairman Paul Volcker adopted a tight-money policy and inflation was squeezed out of the system much faster than almost anybody thought was possible.

But Krugman wants his readers to think that Reagan played no role in this dramatic and positive development.

Samuelson says this is nonsense. Vanquishing inflation would have been impossible without Reagan’s involvement.

What Reagan provided was political protection. The Fed’s previous failures to stifle inflation reflected its unwillingness to maintain tight-money policies long enough… Successive presidents preferred a different approach: the wage-price policies built on the pleasing (but unrealistic) premise that these could quell inflation without jeopardizing full employment. Reagan rejected this futile path. As the gruesome social costs of Volcker’s policies mounted — the monthly unemployment rate would ultimately rise to a post-World War II high of10.8 percent— Reagan’s approval ratings plunged. In May 1981, they were at 68 percent; by January 1983, 35 percent. Still, he supported the Fed. …It’s doubtful that any other plausible presidential candidate, Republican or Democrat, would have been so forbearing.

What’s the bottom line?