–

If You Want Your Team to Win, Support Lower Taxes

Back in 2018, I shared some academic research on the relationship between state tax rates and the performance of professional football teams.

The main takeaway is that teams based in high-tax states did not win as many games, on average, as teams based in low-tax states.

The main takeaway is that teams based in high-tax states did not win as many games, on average, as teams based in low-tax states.

So if you want your favorite team to win, support better tax policy.

Though there are no guarantees. A team from high-tax California just won the Super Bowl, so it goes without saying that taxes are not the only factor that determines team success.

But it presumably means that teams in states like California and New York have to overcome a built-in disadvantage.

Let’s take a look at some new research on this issue. Professor Erik Hembre of the University of Illinois at Chicago authored a study that’s been published by International Tax and Public Finance.

Here’s the question he wanted to answer.

Do higher state income taxes harm firms? …This paper examines the state income tax burden in a unique market, professional sports, where teams—the capital in question—are highly immobile and players—the labor—are highly mobile

to test whether higher state income tax hinders team performance. Anecdotal evidence suggests higher state income taxes disadvantage professional sports teams. Across the four major US sports leagues, of the forty-nine franchises with long championship droughts, only four are from states that do not have an income tax, while twenty are from the highest taxed states.

Here’s his methodology, which takes advantage of the fact that free agency gave players new-found ability to play where they could keep more of their earnings.

To test the link between state income taxes and team performance, this paper analyzes team performance in the four major US professional sports leagues: the National Basketball Association (NBA), the National Football League (NFL), the National Hockey League (NHL), and Major League Baseball (MLB). To address concerns that the association between team performance and income tax rates may be coincidental, I examine how the tax rate effect changed with the adoption of free agency. Achieving free agency has been a milestone for players’ associations, paramount both for increasing player mobility across teams and for forcing teams to compete for player services without restrictions.

Since athletes respond to incentives (just like entrepreneurs, inventors, and scientists), we should not be surprised that Prof. Hembre found that teams in lower-tax states now enjoy more success.

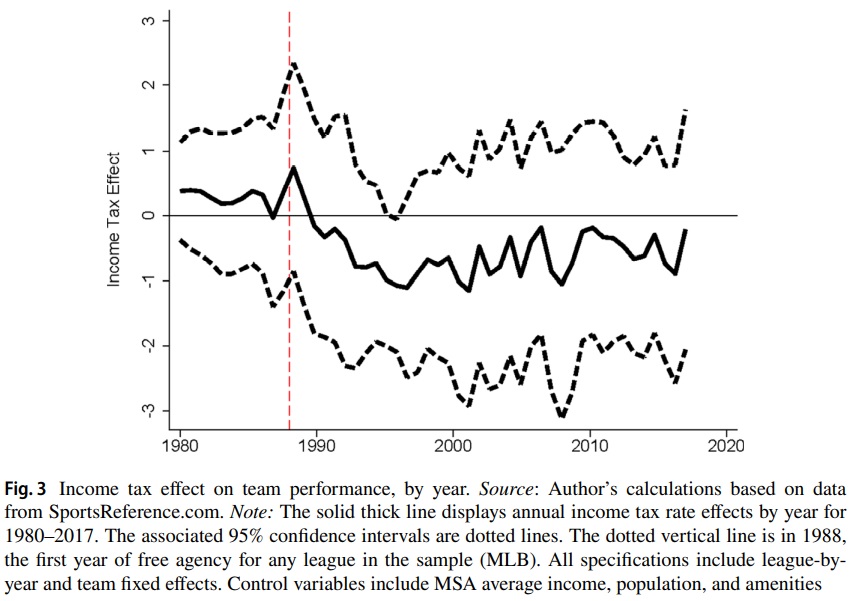

I compare the link between tax rates and team winning percentage before and after the introduction of free agency in each league using within-team variation in top state marginal income tax rates. Prior to free agency, there was a small positive association between income tax rates and winning. After the introduction of free agency, changes in state income tax rates significantly influence team performance. Each percentage point increase in the top marginal income tax rate is associated with a 0.70 percentage point decrease in win percentage. The tax rate effect on team performance is robust to a variety of specifications, such as controlling for sales and property taxes or alternative tax rate measures. Changing the outcome measure to be championships or finals appearances also yields similar results. The estimated effect size is non-trivial. The main analysis effect size of − 0.70 means that a one standard deviation increase in tax rate will result in 2.05 fewer wins over an 82 game season. …Figure 3 presents the annual point estimates (훽2) and 95% confidence intervals of the income tax rate effects between 1980 and 2017. …in all 9 years prior to any league having free agency, there was a positive income tax effect estimate. This relationship changed shortly after the introduction of free agency and since 1990 the annual income tax effect has remained negative.

Here’s the aforementioned Figure 3 for my wonky readers.

As a fan of better tax policy, I like Prof. Hembre’s findings.

As a fan of the New York Yankees, I don’t like his findings

P.S. Here’s one final tidbit that will appeal to fans of the Raiders.

Considering an extreme case, the recent relocation of the Oakland Raiders from a high income tax state (California) to a no income tax state (Nevada) projects a winning percentage increase of 8.6 percentage points or about 1 game per NFL season

P.P.S. I’ll close by reiterating my caveat about taxes being just one piece of the puzzle. After all, I speculated that taxes may have played a role in LeBron James going from Cleveland to Miami many years ago. But he has since migrated to high-tax California. Though many pro athletes have moved away from the not-so-Golden States, so the general points is still accurate.

P.P.P.S. I feel sorry for Cam Newton, who paid a marginal tax rate of nearly 200 percent on his bonus for playing in the 2016 Super Bowl.

P.P.P.P.S. Taxes also impact choices on how often to box and where to box.

P.P.P.P.P.S. Needless to say, these principles also apply in other nations.

The Laffer Curve, Part I: Understanding the Theory

Uploaded by afq2007 on Jan 28, 2008

The Laffer Curve charts a relationship between tax rates and tax revenue. While the theory behind the Laffer Curve is widely accepted, the concept has become very controversial because politicians on both sides of the debate exaggerate. This video shows the middle ground between those who claim “all tax cuts pay for themselves” and those who claim tax policy has no impact on economic performance. This video, focusing on the theory of the Laffer Curve, is Part I of a three-part series. Part II reviews evidence of Laffer-Curve responses. Part III discusses how the revenue-estimating process in Washington can be improved. For more information please visit the Center for Freedom and Prosperity’s web site: http://www.freedomandprosperity.org

___________

After reading Milton Friedman’s book “Free to Choose” in 1980, I had the opportunity in 1981 to hear Arthur Laffer speak about what great economic expansion we were about to have in the USA because of Reagan’s 25% across the board tax cuts on income taxes and sure enough he was right. In fact, our economy expanded so much that the world took notice. Basically from 1980 to 2007 we dropped our top income tax rate from 73% to 39% which is a decrease of 34% and the world saw what we did and followed along. The drop of the industrialized countries during this same time was 26% (from 68% to 42% on average).

Take a look below at this chart:

Table 42.2

Top Individual Income Tax Rates in the OECD (percent)

Change

Country 1980 1985 1990 1995 2000 2005 2007 1980–2007

Australia 62 60 49 47 47 47 45 17

Austria 62 62 50 50 50 50 50 12

Belgium 76 76 58 61 60 53 53 24

Britain 83 60 40 40 40 40 40 43

Canada 64 57 49 49 48 44 44 20

Czech Rep. n.a. n.a. n.a. 43 32 32 32 11

Denmark 66 73 68 64 59 59 59 7

Finland 68 67 60 57 54 53 52 16

France 60 65 60 62 61 56 49 11

Germany 65 65 53 57 56 44 47 18

Greece 60 63 50 45 43 40 40 20

Hungary n.a. n.a. 50 44 40 38 36 14

Iceland 63 56 40 47 45 39 36 27

Ireland 60 65 58 48 42 42 41 19

Italy 72 81 66 67 51 44 44 28

Japan 75 70 65 65 50 50 50 25

Korea 89 65 64 48 44 39 39 50

Luxembourg 57 57 56 50 47 39 39 18

Mexico 55 55 40 35 40 30 28 27

Netherlands 72 72 60 60 52 52 52 20

New Zealand 62 66 33 33 39 39 39 23

Norway 75 64 51 42 48 40 40 35

Poland n.a. n.a. n.a. 45 40 40 40 5

Portugal 84 69 40 40 40 40 42 42

Slovakia n.a. n.a. n.a. 42 42 19 19 23

Spain 66 66 56 56 48 40 39 27

Sweden 87 80 65 50 55 56 56 32

Switzerland 38 40 38 37 36 34 34 4

Turkey 75 63 50 55 45 40 40 35

United States 73 55 38 43 43 39 39 34

Average 68 64 52 49 47 43 42 26

SOURCE: James Gwartney and Robert Lawson, Economic Freedom of the World (Vancouver: Fraser Institute,

2007), as updated to 2007 by the authors. Data includes the national and average subnational tax rates.

NOTE: n.a. not applicable.

___________

I know that Max Brantley and many of his friends over the Arkansas Times like to say that the Reagan tax cuts increased the deficit but that clearly is not true.

President Ronald Reagan’s record includes sweeping economic reforms and deep across-the-board tax cuts, market deregulation, and sound monetary policies to contain inflation. His policies resulted in the largest peacetime economic boom in American history and nearly 35 million more jobs. As the Joint Economic Committee reported in April 2000:2

In 1981, newly elected President Ronald Reagan refocused fiscal policy on the long run. He proposed, and Congress passed, sharp cuts in marginal tax rates. The cuts increased incentives to work and stimulated growth. These were funda-mental policy changes that provided the foundation for the Great Expansion that began in December 1982.

HOW DID THE REAGAN TAX CUTS AFFECT THE U.S. TREASURY?

Many critics of reducing taxes claim that the Reagan tax cuts drained the U.S. Treasury. The reality is that federal revenues increased significantly between 1980 and 1990:

- Total federal revenues doubled from just over $517 billion in 1980 to more than $1 trillion in 1990. In constant inflation-adjusted dollars, this was a 28 percent increase in revenue.3

- As a percentage of the gross domestic product (GDP), federal revenues declined only slightly from 18.9 percent in 1980 to 18 percent in 1990.4

- Revenues from individual income taxes climbed from just over $244 billion in 1980 to nearly $467 billion in 1990.5 In inflation-adjusted dollars, this amounts to a 25 percent increase.

- The Laffer Curve, Part II: Reviewing the EvidenceThis video is second installment of a three-part series. Part I reviews theoretical relationship between tax rates, taxable income, and tax revenue. Part III discusses how the revenue-estimating process in Washington can be improved. For more information please visit the Center for Freedom and Prosperity’s web site: http://www.freedomandprosperity.org.The Laffer Curve, Part III: Dynamic Scoring